Essentials of Cost Recovery at the Canada Energy Regulator (CER)

Essentials of Cost Recovery at the Canada Energy Regulator [PDF 848]

A. Principles

- The Canadian Energy Regulator Act (sec. 87(1)) empowers the CER to make regulations:

- imposing charges to recover costs attributable to its responsibilities, and

- providing for the manner of calculating those charges

- Specifics are set out in the National Energy Board Cost Recovery Regulations (Regulations).

A. Principles (continued)

- Recoverable costs are defined as follows:

CER Operating & Capital costs

PLUS

Cost of services provided without charge to the CER

DEDUCT

“Frontier” costs

= CER Recoverable Costs

- Also not included in recoverable costs

- cost of work and associated overheads performed on behalf of other departments and agencies under Memorandum Of Understanding

- costs specifically excluded by Treasury Board or other authorities (e.g. Arctic Review)

A. Principles (continued)

- Other

- For purposes of cost recovery, the fiscal period is the calendar year.

- The Office of the Auditor General performs an annual audit of CER cost recovery financial statements

B. Concepts

Who Pays What?

- CER cost recovery applies only to CER-regulated companies and facilities

- Cost recovery is premised on commodity charging. This means that costs are allocated to the principal commodities regulated by the CER before being allocated to specific entities within the following sectors:

- Oil - oil pipelines

- Gas - gas pipelines

- Electricity - as of 1 January 2010, international and interprovincial power lines (previously electricity exporters)

- Commodity pipelines (water, steam, CO2) are charged fixed levies

B. Concepts (continued)

Who Pays What?

- Companies pay their share of recoverable costs in 3 ways:

- Levies under the sections .2 and 5.3 of the Regulations, re applied to new companies that are not already regulated by the CER (also known as “greenfield” levies)

- Fixed levies (small, intermediate companies and other commodities)

- Proportional levies (large companies)

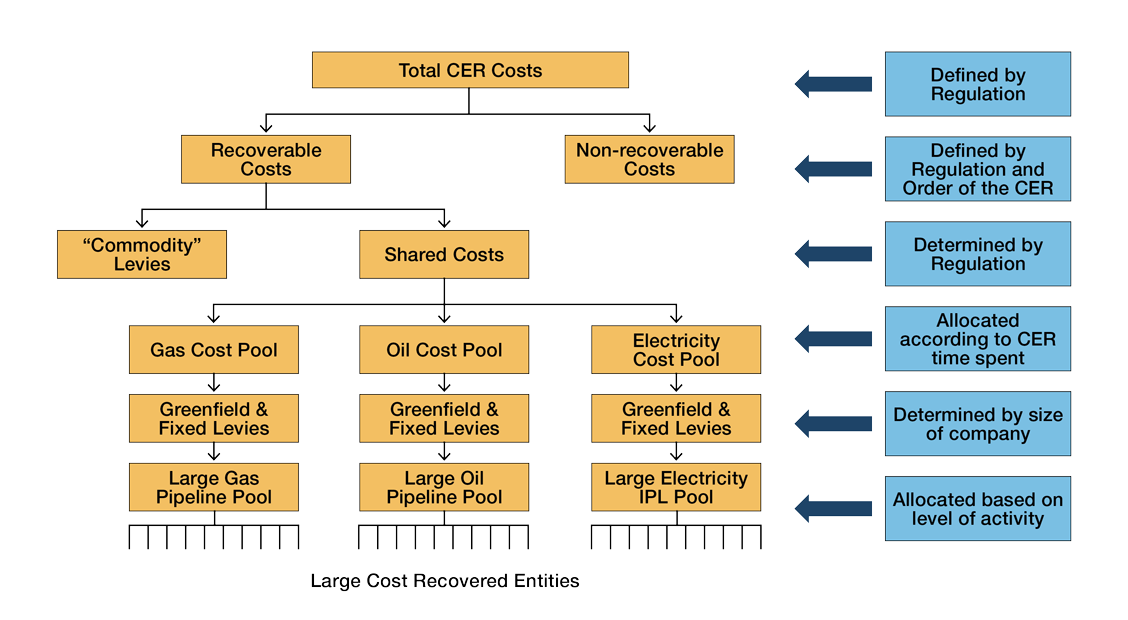

The Allocation "Cascade"

Slide 7 description (click to view)

Flowchart describing the allocation of costs.

- The Total CER Costs defined by Regulation is divided into Recoverable costs and Non-recoverable costs.

- These are defined by Regulation and Order of the Commission.

- Recoverable costs are further divided into Commodity Levies and Shared Costs.

- These are determined by Regulation.

- Shared costs are then allocated into the Gas Cost Pool, Oil Cost Pool, or Electricity cost Pool according to CER time spent on these commodities.

- Fixed levies for small"and intermediate companies as well as section 5.2 and section 5.3 levies are deducted from the relevant commodity cost pool.

- The amounts remaining in the three commodity cost pools are shared by the large companies in those commodity groups according to the activity levels for each company.

B. Concepts (continued)

Who Pays What?

- Allocation Principles

- Allocation of costs to commodity categories is based on time spent on each commodity - gas, oil, electricity

- Within each commodity group, costs are shared according to activity levels (throughputs, transmissions)

C. Billing Processes

1. Obtain relevant company’s operating data by end of August 31 each year

- Throughputs, power line transmissions, and cost of service

- actuals for previous year(s); and

- forecasts for next year

C. Billing Processes (continued)

2. Determine estimate of next year’s recoverable costs for the CER

- obtain CER budgets for current and next fiscal years

- adjust fiscal years to calculate estimated budget for next calendar year

- calculate estimates of recoverable costs for next calendar year

C. Billing Process (continued)

3. Obtain audited results for previous calendar year

4. Calculate difference between previous year’s estimated costs and audited actual costs

5. Determine adjustment (if any) for each company

6. Calculate estimated billing for each company for the coming year - adjusted for differences determined in Step 5

C. Billing Process (continued)

7. Issue information package with preliminary estimated billing information around by end of September each year

8. Receive applications for relief under section 4.1 of the Regulations by end of October each year

9. By end of December each year, issue final estimated billing for upcoming year reflecting reallocations arising from approved applications for relief

C. Billing Process (continued)

10. During the next year, issue quarterly invoices to large companies determined in Step 9 and annual invoice at midyear to small and intermediate companies

Billing Process Summary

DATA ASSEMBLY

CER - costs and time allocation

Company throughputs - forecasts

Actual results from previous year(s) - CER and companies

Create and issue preliminary billing forecast

Receive, review and approve (if eligible) applications for relief under section 4.1 of the Regulations

Issue adjusted billing forecast

Cost Recovery Estimated Billing Process

Slide 15 description (click to view)

Flowchart describing the Estimated Billing Process

- There are two main activities: calculating actual for previous year; and preparing estimates for next year.

- Calculating actuals for previous year:

- OAG audits actual results from previous year and certifies CER recoverable costs

- CER determines cost differences between previous year estimates and previous year actuals

- Difference between estimates and actuals included as an adjustment in billing estimates for next year

- Preparing estimates for next year:

- Companies provide relevant operational and financial data and CER estimates recoverable costs

- CER calculates & issues preliminary billing estimates

- CER receives & decides on applications for relief

- CER issues final billing estimates

D. Other

- Cost Recovery Liaison Committee (CRLC)

- Formal/informal in nature - initiated by the CER and Terms of Reference published in Canada Gazette but no defined membership, structure or processes

- Presently the CRLC consists of industry associations and a few companies

- CRLC meetings are held twice a year, usually at the CER Calgary offices but sometimes elsewhere

- Purposes – to provide a forum to raise issues/concerns relating to cost recovery matters; to discuss the Regulations and accountability reports by the CER; and to discuss upcoming estimates, etc.

- CRLC invites you to consider participation

- Date modified: