ARCHIVED – Canada’s Role in the Global LNG Market – Energy Market Assessment

This page has been archived on the Web

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please contact us to request a format other than those available.

Canada’s LNG Landscape

Current State of North America’s Natural Gas Industry

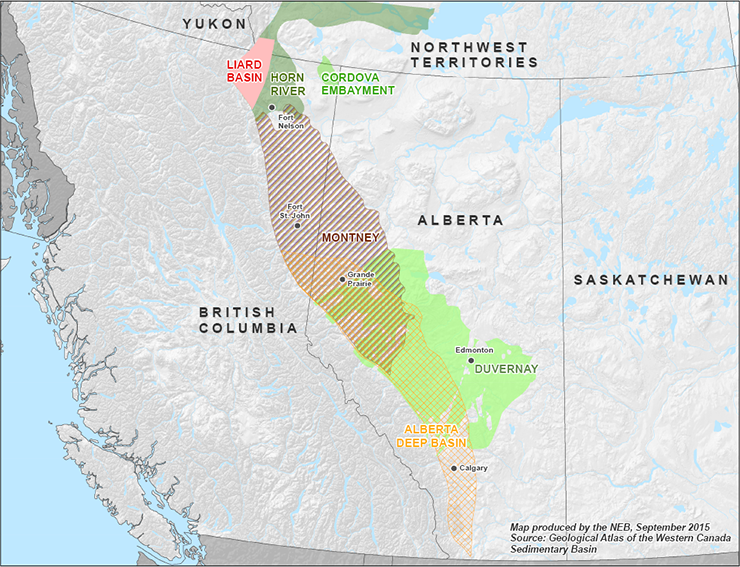

Canada’s natural gas resources are abundant. The total remaining natural gas resource size is 30.8 trillion cubic metres (1012m³) or 1 087 trillion cubic feet (Tcf), with 72% coming from tight and shale gas formations in Alberta and British Columbia. The Montney formation (Figure 2) accounts for 36% of Canada’s total remaining natural gas resources.

Figure 2 – Canada’s Prolific Shale and Tight Gas Resources

Source: Canada’s Energy Future 2016: Energy Supply and Demand Projections to 2040

Description:

This map shows the Montney and Horn River tight/shale plays in north east BC and eastern Alberta which have significant recoverable resources to supply Canadian LNG projects.

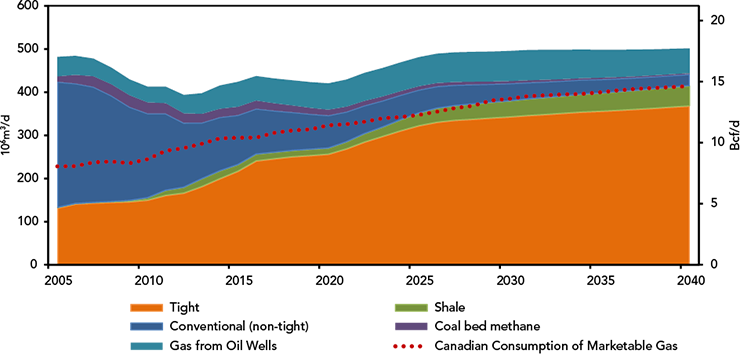

Figure 3 – Canada’s Marketable Natural Gas Production and Consumption

Source: Canada’s Energy Future 2016: Update – Energy Supply and Demand Projections to 2040Footnote 1

Description:

This stacked area chart shows Canada's projected natural gas production growth from tight/shale resources, tight gas is the major contributor of growth to 2040. While Canada's gas demand is expected to increase, there will be production surplus to Canadian needs that can be exported via LNG or other transportation modes.

Technological advances in horizontal drilling and hydraulic fracturing have led to the development of tight and shale resources. Previously uneconomic to develop, tight and shale resources are now more than half of current production and the main areas of future growth for Canadian natural gas supply (Figure 3). The NEB projects that production in Canada will increase by 18% by 2040.

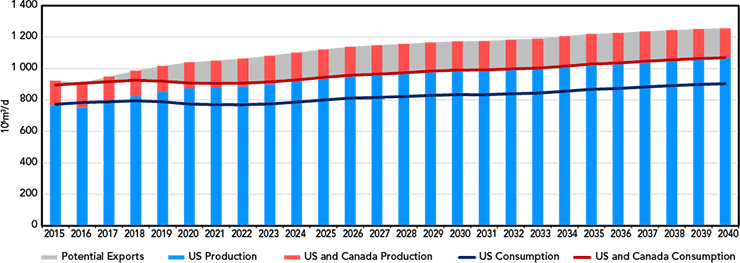

The same technologies have resulted in the development of U.S. shale resources, which are even larger than Canada’s. The U.S. Energy Information Administration (EIA) projects natural gas production to increase 40% in the U.S. by 2040. As shown in Figure 4, combined Canadian and U.S. production is expected to exceed combined consumption beginning in 2017.

Figure 4 – Canada and U.S. Natural Gas Production and Consumption

Source: Canada’s Energy Future 2016: Update – Energy Supply and Demand Projections to 2040, EIA (Annual Energy Outlook 2017)

Description:

This chart shows U.S. production of natural gas is projected to increase at a faster rate than Canadian production of natural gas. Consumption of natural gas in both the U.S. and Canada is pojected to increase steadily. By 2024, U.S. production alone is projected to match total consumption in both the U.S. and Canada.

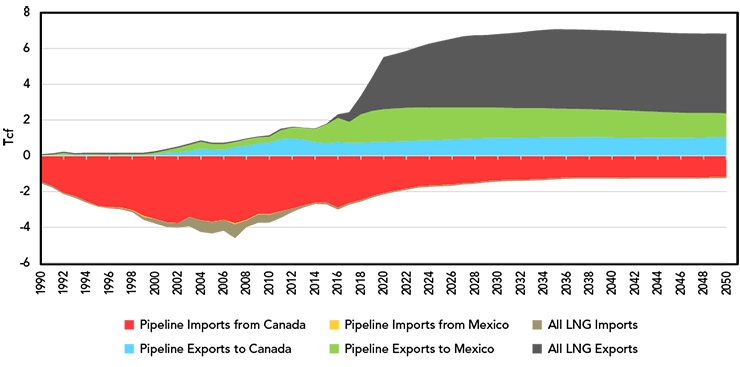

Canada has always been a net natural gas exporter, with nearly all exports going via pipeline to the U.S. However, in recent years U.S. demand for Canadian gas has decreased due to increases in U.S. production. Historically the U.S. has been a net importer of natural gas but is set to become a net exporter in 2017/2018. As shown in Figure 5, natural gas exports from the U.S. are set to triple in the next three years; LNG exports are projected to surpass pipeline exports.

Figure 5 – U.S. Natural Gas Trade

Source: EIA (U.S. Natural Gas Exports and Re-Exports by Country, U.S. Natural Gas Imports by Country)

Description:

This chart shows that natural gas imports to the U.S. are nearly zero, and pipeline imports from Canada to the U.S. are projected to decrease. LNG exports from the U.S. are projected to grow to 7 trillion cubic feet by 2040.

Current State of Canada’s LNG Industry

Canada has one existing large-scale LNG regasification (import) terminal, the Canaport LNG facility in New Brunswick, which began operating in 2009 and has a capacity of 34 106m³/d (1.2 Bcf/d)Footnote 2. Canaport LNG receives offshore supply from regions such as the North Sea and the Caribbean, and helps supply the natural gas needs of Atlantic Canada and the U.S. Northeast via the Emera Brunswick Pipeline. Due to changing natural gas market dynamics in North America, Canaport LNGs owners, Repsol and Irving Oil, initially proposed to convert the LNG import facility into an LNG export facility and received a 25-year export licence from the NEB. However, the project’s proponents announced that the project is currently on hold.

Figure 6 – Canaport LNG Facility

Source: Canaport LNG

While Canada is not yet involved in large-scale global LNG export trade, Canada’s LNG industry dates back decades. It is comprised primarily of small-scale liquefaction and regasification facilities that serve local markets. LNG is used to smooth or peak shaveFootnote 3 fluctuating demand on natural gas pipeline systems by liquefying and storing gas in specialized storage tanks when demand is low, and then regasifying and supplying gas when demand is high. LNG plants such as FortisBC’s Tilbury Facility and Gaz Metro’s LSR Montreal plant currently serve as peak shaving facilities in addition to selling LNG to industrial customers, and both are expanding their capacity.

In remote areas with no gas pipeline infrastructure, LNG is transported by tanker truck to serve industrial customers operating heavy drilling and mining machinery, to power gas-fired electrical generating stations, and to serve as heating fuel in rural communities. LNG is also used in Canada to fuel ferries and ships.

Proposed Canadian LNG Projects

Under the National Energy Board Act (NEB Act), the Board must authorize all exports and imports of natural gas from Canada, including LNG. Proposed LNG projects must also receive regulatory and environmental approvals from other federal and/or provincial regulators. The final investment decision for each LNG project lies with the project proponents’ management, and is usually based on a combination of market and regulatory factors.

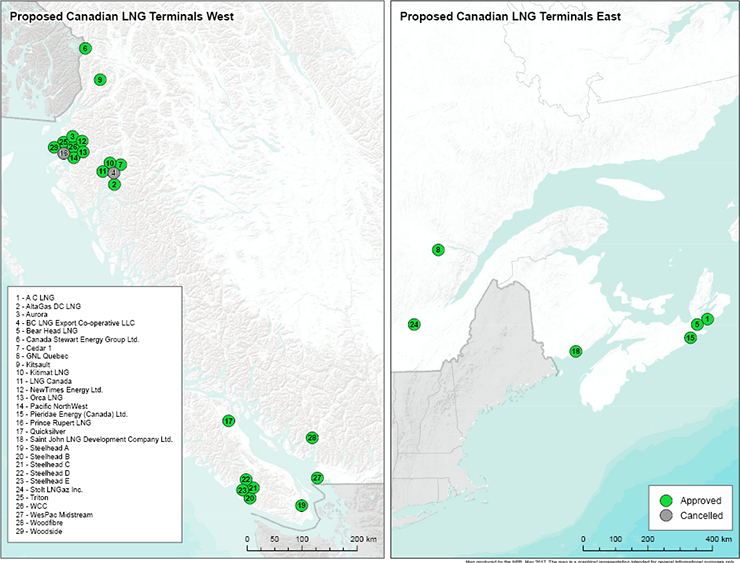

Since 2010, the Board has received 43 LNG export licence applications, 35 of which were approved. There are 24 distinct projects, with 18 projects based along the B.C. Coast and the remaining projects located in the Maritimes and Quebec. Figure 7 shows the geographical location of the proposed facilities associated with the approved licences.

These applications were largely for the export of LNG from western Canada to Asian markets, although there were also applications to ship gas from eastern Canada to the Atlantic basin (Europe/Latin America) and Indian markets. Four east coast projects have also been granted import licences to accommodate the movement of gas across the border from the U.S. The projects range in size from 2.3 103 m3/d (0.08 Bcf/d) to 130.2 106 m3/d (4.6 Bcf/d). See Appendix 1 for a list of all licences approved by the Board.

Figure 7 – Canadian LNG Export Licences Approved for Proposed Projects

Source: NEB

Description:

These two maps show that west coast Canada has many more LNG projects with approved exports licences versus the eastern coast of Canada, largely due to west coast advantages of large gas supply access and proximity to Asia.

There are more proposed LNG projects on the West Coast than on the East Coast. This is because there is significant gas supply in northeast B.C. and Alberta and many of the largest LNG project proponents are also gas producers in western Canada aiming to maximize the value of their producing assets by seeking alternate markets.

Secondly, the West Coast is a shorter distance to the primary target market of Asia. Consistent with this, many proposed Canadian LNG projects have investors from countries such as Japan, Korea, China, and India. Some of these Asian proponents have already entered into long-term contracts with their project partners to buy a portion of the Canadian-produced LNG. These long-term contracts are important to the viability and financing of larger Canadian LNG projects, as these would be costly greenfieldFootnote 4 developments.

A small number of projectsFootnote 5 on Canada’s west coast have received regulatory approvals but most are waiting for market conditions and project economics to improve before reaching a final investment decision (see Appendix 1). In Quebec, one project received regulatory approvals to proceed but has not moved the project forward. On the East Coast, one project received regulatory approvals from all levels of government, but project proponents are working to secure gas supply before proceeding.

The competitive nature of global LNG markets means that not all proposed LNG projects are likely to be built. To date, none of the LNG export facilities associated with NEB export/import licence approvals have reached the construction stage, although dozens of LNG projects are at various stages of planning. Only one of these projects, Woodfibre LNG has reached a final investment decision. Woodfibre LNG is being built on a repurposed site (formerly a pulp mill) near Squamish B.C. It is one of the smaller volume NEB export licence holders, with a 40-year licence to export up to 2.1 million metric tonnes per annum (MMtpa) (0.3 Bcf/d) of LNG.

- Date modified: