ARCHIVED – Optimizing Oil Pipeline and Rail Capacity out of Western Canada - Advice to the Minister of Natural Resources

This page has been archived on the Web

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please contact us to request a format other than those available.

March 2019

Copyright/Permission to Reproduce

ISBN 978-0-660-29867-2

A. The National Energy Board’s advice

Canada’s Minister of Natural Resources requested advice from the National Energy Board (NEB or Board) on three key questions. The Board’s advice is summarized here, with details following in the remainder of the report.

1. Is the current monthly nomination process to access available capacity on oil pipelines functioning appropriately, consistent with the “common carrier” provisions of the National Energy Board Act and efficient utilization of pipeline infrastructure (for example, by auctioning uncontracted export capacity to smaller producers)?

The Board advises that pipelines transporting crude oil out of western Canada are currently operating at their full capacity, after recent optimization efforts from pipelines and their shippers. Any notable increase in pipeline throughput would need to come from new capacity additions, rather than further optimization of existing pipeline systems. Unexpected delays in almost all proposed major pipeline projects in the last decade have resulted in oil production surpassing pipeline capacity, creating an extended period of high levels of pipeline apportionment.

In the current circumstances, the existing monthly nomination procedures on the four major crude oil export pipelines do not appear to affect the pipelines’ operational efficiency. Additionally, the information gathered by the NEB in preparing this advice does not raise compliance concerns with respect to nomination and verification rules specified in tariffs on NEB-regulated pipelines, which are in place to help satisfy common carriage requirements. However, existing verification procedures across the industry as a whole allow shippers to nominate more oil to pipelines than can be supplied. Integrated producers and those shippers that own or have contracted crude oil storage and refinery capacity have a greater ability to acquire pipeline capacity. These shippers made certain investments in the past and, under current market conditions, these investments provide more flexibility in accessing pipeline capacity.

During consultations, there was a lot of discussion on the current method of allocation and whether, in effect, it complies with the spirit of common carriage. Although it would involve facilities outside of the jurisdiction of the NEB, improving the existing verification framework through the whole supply chain may address these concerns. Any change to the way shippers access pipeline capacity would have significant effects on markets and stakeholders. Accordingly, consultation with stakeholders would be needed.

Changes to existing nomination or verification procedures would reallocate pipeline space among shippers, but would not increase utilization further. A more direct way to address pipeline access issues would be additional pipeline capacity.

2. Are there any other impediments to the further optimization of pipeline capacity that could be addressed by the National Energy Board, governments or pipeline companies, in the short-term and long-term?

The Board advises that there are several potential solutions to further optimizing capacity, but most of them would require structural changes to the market, significant investments, and a long time horizon. For example, building partial upgraders could reduce the amount of diluent needed to ship bitumen, freeing space in existing pipelines. Reversal of existing pipelines currently importing diluent could increase the amount of oil exported from western Canada. However, uncertainty regarding if and when incremental pipeline capacity will come online has ripple effects across industry by hampering investment decisions to develop alternatives to pipelines, including addition of rail capacity.

Private investors may be reluctant to make major investments in projects that may become uneconomic if new pipeline capacity is added. However, in making investment decisions, governments may have different motives than private investors, such as increasing market diversification, employment, and government revenues.Footnote 1

The Board also advises that governments may have a role to play in enhancing transparency of the market by collecting and publishing non-public market data in a timely manner to create a more level playing field for all market participants.

3. Are there short-term steps to further maximize rail capacity that could be addressed by governments to alleviate the current situation?

The Board advises that rail is not a perfect substitute for additional pipeline capacity. Moving crude by rail is more expensive and becomes less economic if price differentials narrow. It also typically involves a more complex process than moving crude by pipeline. Additionally, arranging transportation for crude by rail has a long lead time and impacts shipment of other goods. Uncertainty about the timing and approval of additional pipeline capacity is hampering private investment in rail capacity. There may be a role for governments to simplify or coordinate the process for arranging rail transportation, especially for smaller companies that may not be able to make long-term financial commitments. However, any policy action has the potential to create unintended consequences given the complexity of the system.

The Board thanks the Minister for this opportunity to provide input on these important issues.

B. Introduction

On 30 November 2018, Canada’s Minister of Natural Resources, the Honourable Amarjeet Sohi, wrote to the NEB to seek advice on options that may exist to further optimize pipeline capacity out of western Canada.Footnote 2 This was in response to the wide price differentials for Canadian crudes in the latter part of 2018, and their impacts on Canada.

The NEB released a report, Western Canadian Crude Oil Supply, Markets, and Pipeline CapacityFootnote 3, on 27 December 2018.

In January 2019, NEB staff held thirty meetings with selected pipeline companies, producers, shippers, associations, government agencies, and other experts to seek input on the questions in the Minister’s letter. The Board thanks the following companies and organizations for meeting with Board staff and providing input on the issues:

- Alberta Energy

- Altex Energy

- ARC Energy Research Institute

- Athabasca Oil Corporation

- BP Canada

- C.D. Howe Institute

- Canadian Association of Petroleum Producers

- Canadian National Railway

- Canadian Natural Resources Ltd.

- Canadian Pacific Railway

- Canadian Transportation Agency

- Cenovus Energy Inc.

- ConocoPhillips Canada

- Crescent Point Energy

- Crude Oil Logistics Committee

- Devon Canada Corporation

- Enbridge Inc. for the Enbridge Mainline

- Explorers and Producers Association of Canada

- Express Pipeline Ltd.

- Gibson Energy

- Imperial Oil Limited

- Japan Canada Oil Sands Limited

- Marathon Petroleum Trading Canada LLC

- MEG Energy Corp.

- Suncor Energy Inc.

- Torq Energy Logistics

- TransCanada Keystone Pipeline

- Trans Mountain Pipeline

- Transport Canada

- Vermillion Energy

The NEB launched an online forum to gather input from 27 December 2018 through 18 January 2019, and received 16 submissions from the public. In addition to these meetings and submissions, Board staff also spoke with consultants and academics to supplement the Board’s in-house knowledge in preparation for this report.

C. Markets

The NEB released a report, Western Canadian Crude Oil Supply, Markets, and Pipeline Capacity, on 27 December 2018. That report provides market context for this advice to the Minister. The NEB recommends reading that document together with the additional market context presented here.

Global oil markets operate competitively, however they are extremely complex with:

- varying levels of transparency

- many different types of crude oil and refined products

- limitations on the types of crude oil that refineries can accept

- multiple trading platforms, contracts, and timeframes

- numerous ways of transporting crude oils and refined products, all of which can be constrained

- varying degrees of market regulation across multiple jurisdictions

- numerous local and regional market dynamics.

As discussed in the report issued in December, western Canada produces far more oil than it can consume or store locally. Therefore, oil must be exported. The United States Midwest and Gulf Coast are some of the largest markets for Canadian oil and therefore these markets determine the prices Canadian producers receive for their oil. This makes Canadian producers “price takers”.

Recent prices and market impacts

Western Canadian oil prices have significantly recovered and price differentials with WTI narrowed since last fall, though this is largely because of Alberta’s production curtailment.

Canadian crude prices have recovered since last fall when the most commonly quoted Canadian oil benchmark, Western Canadian Select priced at Hardisty, Alberta (WCS), traded at a record discount of more than US$50 per barrel relative to West Texas Intermediate priced at Cushing, Oklahoma (WTI).Footnote 4 Price differentials slightly narrowed in late November and early December, and further narrowed when the Government of Alberta announced its production curtailment. In mid-January, the WCS-WTI discount reached US$7.50 per barrel.Footnote 5

January’s differentials narrowed further than many producers, marketers, and other industry experts had expected. While supply has decreased due to mandated oil production curtailment, pipelines are still full and early indications are that storage levels remain relatively high.Footnote 6

Current WCS-WTI differentials of approximately US$10 per barrel are below the cost to ship crude by rail to major refining markets in the United States. Transporting crude from Alberta to United States refineries by rail typically costs US$15-22 per barrel, and business decisions to ship by rail are made anticipating differentials in this range. As a result, when differentials are quite narrow, less oil tends to leave Alberta by rail. Shippers prefer to move their oil by the least expensive mode of transport available, which is pipelines.

Market data issues

Better public data regarding storage, refining, and pricing could help the crude oil market work more efficiently.

For the transportation of oil to be efficient, all parts of the supply chain must work together. Contractual flows of oil are such that a barrel may be bought and sold a number of times. A barrel of oil may be purchased by several marketers and other third parties before reaching the refinery where it is consumed. Oil can be transferred by:

- A producer selling directly to a refinery

- An integrated producer supplying its own refinery

- A producer selling to a marketer or other third parties, who may sell it to other parties in a series of transactions ending at a refinery

An integrated producer may do all of the above.

Integrated producers produce oil and own refineries. Non-integrated producers sometimes enter long term contracts with refineries. This gives them options similar to those of integrated producers.

Larger producers (including integrated producers) may have marketing departments that find downstream refiners to buy oil production. Producers may also sell directly to a marketer, who then takes on the risk of finding another buyer, whether it is another marketer or a refinery. Alternatively, some producers may pay a fee to have marketing companies sell their production on their behalf. In particular, smaller producers tend to use this option. When the price differential is wide, producers are better off exporting their crude oil to markets where the price is higher. If they cannot get access to these markets they earn less profit or may even be forced to sell at a loss.

When markets have limited information, different market participants may not be able to make informed decisions. Some public data are available for some aspects of the oil supply chain in western Canada, though transparency could be improved. For other aspects, commercial datasets are available at a cost and often have significant restrictions on publication.

Additional information could be made available to the public through frequent and timely publishing of transparent data such as, but not limited to:

- daily benchmark oil prices in Canada and the United States, including differentials

- weekly oil storage capacity and inventories

- weekly or monthly crude by rail capacity, loading and shipments

- monthly oil imports and exports

- pipeline nominations and apportionment

Better refinery data – such as inputs of crude oil and outputs by product – could also be useful, though the data would need to be treated carefully given the regional and increasingly concentrated nature of the sector.Footnote 7 Gathering and publishing more refinery information could put commercial business positions at risk, though data could be aggregated to help mitigate this (e.g., by region).

Additional data could help market participants in a variety of ways. For example, if small producers knew storage was almost completely full or that refineries were shut down, then they could anticipate not being able to sell or store their product, and might decide to reduce production. Data regarding refinery crude runs and refinery outages would also be beneficial for most market participants for planning purposes. More detailed apportionment data would help producers better understand the volume of oil being “pushed back”Footnote 8 to them by apportioned shippers.

Providing more public data on oil markets could be a near-term improvement. Most market participants do not have any incentive to provide data to the public, but greater information makes markets work more efficiently. Therefore, governments may choose to step in although making data freely available to the public may negatively affect existing commercial-data providers. Provinces regulate their energy infrastructure and could require reporting for various levels of storage, from field level to hub level. Provinces could also supply an aggregate of the energy-price data they use for royalty calculations.

Canadian and United States oil markets are integrated with one another, meaning that publishing Canadian datasets similar to United States datasets may also be beneficial. For example, the Energy Information Administration of the United States publishes daily oil prices as well as weekly storage and refinery input and output data, all of which are widely used by industry, governments, and the public. The Government of Canada has shown an interest in providing more energy information to Canadians. Statistics Canada is also authorized to collect a wide variety of information. Thus, the Government of Canada may also be well positioned to collect and publish this information.

D. Pipeline capacity

Existing export pipelines are fully utilized. Any significant increase in throughput would need to come from new capacity additions rather than optimization of existing pipeline systems.

Capacity and utilization

The average utilizationFootnote 9rate on the country’s major export pipelines - Enbridge Mainline, Keystone, and Trans Mountain - was 98% in the last quarter of 2018.

Several pipeline projects out of western Canada have been proposed in the last decade, but many projects have been cancelled or delayed. The table below lists oil pipelines out of western Canada that were proposed, their proposed capacity increase in thousand barrels per day (b/d), the year the project proponents initially expected the pipeline to go into service, and the current status of each proposal.

| Proposed pipeline project | Capacity increase (thousand b/d) | Original proposed in-service date | Status |

|---|---|---|---|

| Keystone XL (TransCanada) | 830 | 2012 | The company intends to complete construction of the Canadian portion by 2020. In the United States, timing is uncertain due to regulatory challenges. |

| Northern Gateway | 525 | 2016 | Did not proceed; Government of Canada directed the NEB to dismiss the application. |

| Trans Mountain Expansion | 590 | 2017 | The NEB recommended approval in February 2019, pending Governor in Council decision. |

| Energy East | 1100 | 2017/18 | Application withdrawn [Filing A86594]. |

| Line 3 Replacement (Enbridge) | 370 | 2018 | Canadian portion in construction and expected to be complete in 2019. Coming into service and final throughput dependent on United States’ portion. |

Oil production in western Canada has steadily increased since the early 1980s. Historically, pipeline capacity has grown along with production. Capacity is added in large increments as new pipelines or major expansions occur, so the market would move from having a small amount of excess pipeline capacity to a larger amount.

Producers, particularly those with a focus on oil sands, invested with a long-term view and with an expectation that sufficient pipeline capacity would be available. Oil production has now outgrown pipeline capacity, causing apportionment that market participants expect to last until new pipeline capacity is put into service. Lack of sufficient pipeline capacity has made it difficult to ship oil out of western Canada, and prices have plunged, substantially reducing revenues for some producers and shippers and reducing government royalties and other revenues.

Apportionment sometimes happens when there are temporary market disruptions, or constraints imposed by pipeline maintenance or operating conditions. Apportionment may also result from many producers or shippers all trying to reach the highest priced market. In the past, even if shippers could not reach a preferred market, they could still get capacity on other pipelines to move oil out of western Canada. More recently, however, shippers are facing excess oil supply in western Canada relative to local demand, pipeline capacity, rail capacity, and available storage and have nowhere to move their oil.

Optimization

Some operational issues have affected pipeline utilization in the past. These do not appear to be issues now.

Operational complexity

Due to operational complexity, it is not possible for any pipeline to operate at 100% of capacity on a sustained basis. Some pipeline systems, such as the Enbridge Mainline, are inherently more difficult to operate at full capacity due to their size and the complexities of managing flows across multiple lines.

In recent years, pipeline companies have incrementally increased capacity and throughputs on their pipeline systems. For example, with the cooperation of its shippers, Enbridge Mainline improved its scheduling. This improvement was due to the introduction of a supplemental policy to fill under-utilized pipeline space. It increased the amount of usable capacity on the pipeline through quality pooling (where similar types of crude are grouped into common pools), making pipelines more flexible in transporting different qualities of crude oil. Some pipelines also increased total capacity through small investments in new facilities. While further operational improvements may be possible, they are unlikely to result in material pipeline capacity increases out of western Canada.

Batching

Oil pipelines typically ship products in batches, because different commodities must be kept separate from one another to minimize contamination. For example, the Enbridge Mainline ships dozens of commodities, including some refined petroleum products. Shipping batches of various commodities increases the complexity of scheduling receipts and deliveries compared to moving a single commodity. However, systems have mitigated some inefficiencies by optimizing quality pooling rules, as recently done by Enbridge and its shippers. It is possible that pipelines could further optimize quality pooling rules, but shippers might not agree as they value their commodities differently.

Change requests

Oil storage

Oil physically flows from producers to refiners in a variety of ways, and can be stored when required. Storage facilities can be found near producing sites upstream, linked to feeder and large export pipelines, or located downstream at refineries. Storage helps pipeline companies balance short-term supply and demand fluctuations on the pipeline network. Additionally, storage can maximize value for the crude by delaying delivery until buyers are ready for it or prices increase.

Some pipelines experience a large number of in-month change requests for shipper nominations. A change request could be, for example, a change to the shipping destination. Pipeline operators indicated that these requests do not typically impact throughputs. For instance, if the pipeline is connected to a large inventory of crude oil in storage, it is less likely to miss opportunities to ship batches. Therefore, storage can increase the operational efficiency of a pipeline by reducing the risk of lower throughput. Pipelines may also decline change requests that will impact network operations. While these change requests have been problematic in the past, pipeline companies have largely resolved these issues.

E. Allocating pipeline capacity

Existing pipeline takeaway capacity is being fully and efficiently utilized from an operational perspective.

Many different shippers are competing for access to the limited available pipeline space. These shippers include: refineries in the United States seeking to ensure that they will have reliable supplies for their operations; producers looking to sell their production at attractive prices in export markets; as well as marketers and other companies that may buy oil from any number of parties to move it to markets outside western Canada. While overall capacity is being fully utilized, some market participants have raised concerns regarding how pipeline capacity is currently allocated among shippers.

Procedures for allocating pipeline capacity

Pipeline tariffs specify the procedures by which shippers are to submit nominations for transportation service, including the form and timing of nominations. The tariffs also set out the rights and authorities of pipeline companies to verify nominations. The NEB regulates and determines compliance with tariffs for pipelines under its jurisdiction, which include the major export pipelines from western Canada. Pipeline companies and shippers are required to follow the rules and regulations of transportation service as set out in the tariffs.

Nomination procedures

Access to pipeline capacity is obtained by submitting nominations to move crude oil on a pipeline.

A shipper must submit nominations each month to each pipeline or facility that its oil flows through. This includes gathering lines, feeder lines, storage terminals, and large export pipelines. In its nomination, the shipper will specify the volume and type of crude oil that it intends to ship the next month, and the receipt and delivery points. Shippers must submit nominations for both committed (or contracted) transportation service, if available, as well as uncommitted transportation service. Nominations on each pipeline and facility are typically due on the same dates and times.

Apportionment is the percentage by which each shipper’s nominated volume is reduced to meet the pipeline’s uncommitted capacity. Generally, apportionment is applied equally across all shippers seeking to use that capacity. For example, if shipper A nominates 100 barrels and shipper B nominates 1000 barrels, then, under 10% apportionment, shipper A will be able to ship 90 barrels, and shipper B will be able to ship 900 barrels.

Based on operating conditions, each pipeline operator determines the available capacity of its pipeline for the month. Pipelines first allocate capacity to committed shippers based on the committed shippers’ verified nominationsFootnote 10 (up to their committed capacities). Any remaining capacity is treated as uncommitted capacity. If remaining nominations exceed remaining capacity, there will be apportionment on the pipeline. Under apportionment, uncommitted capacity is typically allocated on a pro rata basis, whereby each shipper is allocated a proportional share of pipeline capacity based on its verified nominations.

After the pipeline operator builds its shipping schedule using the accepted nominations, shippers may submit change requests to revise various aspects of the accepted nominations, as discussed in Section D.

Verification procedures

Verification is performed to ensure that a shipper has the capability to satisfy its nominations.

To ensure that a shipper has not nominated volumes that it cannot deliver to the system, the pipeline may require certification that the shipper has available supply sufficient to fulfill its nominated volume. The pipeline may also require certification that the destination facility is capable of accepting the shipper’s nominated volume.

Verification is not limited to NEB-regulated pipelines and may occur at any facility that receives nominations from shippers. For example, feeder pipelines, storage terminals, and downstream connecting pipelines and other facilities may all verify the nominations they receive. As part of the verification process, a facility may request verifications from both upstream and downstream connected facilities.

The NEB does not mandate the verification of shipper nominations, and it has generally allowed pipeline companies to develop and administer their own verification procedures. Accordingly, NEB-regulated pipelines conduct the following types of verification:

- Enbridge uses three types of verification on the Enbridge Mainline. First, supply is verified by requiring each shipper to submit a certificate, executed by an officer of the shipper company, confirming that the shipper has the capability and intent to tender each crude type and volume, and that the nomination has not been inflated to factor in apportionment. Second, volumes must be verified by the connecting upstream facility. Third, each downstream destination facility must submit monthly verification affidavits, attesting that it is capable of receiving, and intends to receive, the crude oil volumes nominated to it.

- Express Pipeline verification procedures generally follow those used on the Enbridge Mainline, with the exception of the shipper certificate and destination verification. The majority of throughputs on Express Pipeline flow through the interconnected Platte Pipeline in the United States. Platte allocates its capacity to shippers before Express conducts its own allocation procedures. Pursuant to the delivery verification procedures in the Express Pipeline tariff, the allocations on the Platte Pipeline limit the nominations that are accepted for each shipper on the Express Pipeline.

- Trans Mountain uses different types of verification, depending on the circumstances. For each shipper’s nomination, Trans Mountain requires written third-party verification from the interconnected upstream facility that the shipper has the capability to tender product to satisfy its nominated volume. Trans Mountain also requires written third-party verification from the downstream delivery destination that the shipper has the capability to remove its nominated volume from the pipeline. If a shipper cannot provide upstream verification or destination verification from unaffiliated third parties, Trans Mountain requires the shipper to provide a certificate executed by an officer that addresses both supply and destination verification.Footnote 11

- Keystone seeks verification (in the form of upstream and downstream verification) of a shipper’s nomination only when Keystone deems that it has reasonable grounds to do so. These verifications may occur if a shipper has failed to use the pipeline capacity that it was allocated in the previous month or failed to provide Keystone with sufficient notice regarding cancelled batches. In effect, this allows a shipper on Keystone to nominate up to the entire pipeline capacity, subject to Keystone determining that the shipper has proper credit in place to pay the transportation tolls for the resulting allocated volume.

Current issues in allocating pipeline capacity

The information gathered by NEB staff in preparing this report raises no concerns relating to shippers’ compliance with the nomination and verification procedures that may be set out in NEB-regulated pipeline tariffs. However, several industry participants raised concerns regarding how pipeline capacity is allocated among shippers. In general, these concerns revolved around the effectiveness of verification procedures throughout the supply chain and the potential for shipper over-nominations.

Evidence of over-nominations

There is evidence of over-nominations on the four major export pipelines.

In the current environment of constrained pipeline capacity, some shippers nominate more barrels of oil than they intend to ship. While shippers are complying with the procedures that are specified in NEB-regulated tariffs, over-nominations have occurred on the four major pipelines that export oil out of western Canada.

To illustrate this, in December 2018, more than 13 million b/d of oil were nominated for shipment on pipelines exporting oil from western Canada. However, the total amount of oil supply available for exportFootnote 12 in that month was approximately 5.4 million b/d.

Causes of over-nominations

Integrated and transparent oversight of nomination and verification procedures are lacking across pipelines and other facilities.

By over-nominating, shippers increase the likelihood that, after apportionment, they receive the amount of pipeline capacity they desire. Over-nominations may also provide these shippers with excess capacity, and an opportunity to fill this capacity with lower-priced crude that is stranded in the local market.

Verification can serve to limit over-nominations. With effective verification, the total nominations to all export pipelines should not exceed reasonable forecasts for production and what could reasonably be removed from storage in a given month.

However, existing verification procedures do not appear to be limiting over-nominations in this manner. This is largely due to the fact that while the crude oil supply chain is integrated from an operational perspective (i.e., it facilitates the flow of crude oil from production site to end destination), the oversight of nominations and verifications is not integrated across all facilities in the supply chain.

Currently, verification is not mandated by regulators or governments and is at the discretion of the facility operator. For example, during its consultations with industry participants, the NEB heard that one major export pipeline and many upstream feeder pipelines and terminals do not always verify shipper nominations. Additionally, there is no requirement for facilities to follow the same or similar verification procedures across industry. The Crude Oil Logistics Committee has created verification guidelines for all facilities upstream of major export pipelines; however, the effectiveness of the guidelines has been limited thus far by voluntary participation and the lack of an enforcement authority.

The Crude Oil Logistics Committee (COLC) is made up of over 90 organizations, including producers, shippers, pipelines, terminals, industry associations, and government regulators and departments. In 1996, the COLC developed an industry-wide standard for supply forecasting and nomination procedures. The procedures cover all parties upstream of the major pipelines or export pipelines, including gathering pipelines, feeder pipelines, shippers, and terminal operators.

The goal of the procedures is to ensure there is a reasonable level of accuracy in supply forecasting, each system is balanced (receipts and dispositions), transfers from one system to another match, and to ensure there is no overlap or gap in volume forecast data from system to system.

Feeder pipelines ultimately provide large export pipelines with verified forecasts of deliveries which are the result of the supply forecasting and disposition data.

Moreover, there is no rigorous verification system that would help ensure that each barrel of crude oil produced is ultimately nominated to just one destination. The market and supply chains are complex, and each barrel of crude oil may have been purchased and sold by several different companies and traveled through several different facilities before it reaches its ultimate destination. Accordingly, NEB-regulated pipelines rely on upstream facilities to provide verification data to be used in verifying shippers’ nominations to the pipeline.

Some upstream facilities do not provide the data that would allow verification, sometimes due to confidentiality agreements between facility operators and users. Consequently, the lack of coordination and flow of data between facilities creates challenges for major export pipelines in verifying nominations.

Without nomination and verification data, facility operators may be able to assess whether shippers have the physical capability to satisfy their nominations. However, they may face significant challenges in determining whether a shipper has the intent to transport the barrels that they have nominated. For example, a company that owns or contracts storage may nominate to a pipeline the full amount of oil that it has in storage, even if it does not intend to move this oil and instead hopes to purchase lower-cost supply just prior to the shipping date. The pipeline may determine that the shipper’s storage facility has the capability to satisfy the shipper’s nominated volume, but the pipeline may not be able to verify that the shipper does not have the intent to ship the volumes nominated from its storage facility.

Impacts of over-nominations

Under current verification procedures, integrated producers and shippers who own or have contracted storage and refining capacity have greater ability to acquire pipeline capacity. Over nominations may result in producers selling their crude oil at reduced prices.

Over-nominations have resulted in high levels of apportionment, and have had several impacts on participants in the Canadian oil industry.

First, over-nominations have contributed to some western Canadian producers selling their crude oil at depressed prices. When shippers over-nominate to pipelines, apportionment is exacerbated. Contracts in place between producers and shippers are structured such that a shipper is able to “push back” apportioned barrels to the producer. As apportionment levels increase, more barrels can be pushed back to producers. This sudden, artificial increase to the oil supply in the local market can cause western Canadian crude prices to become severely depressed, particularly when producers lack access to adequate storage. Consequently, producers receive materially lower prices for their crude oil.

Shippers that over-nominate and have remaining allocated pipeline capacity can then buy oil at substantially reduced prices in this market. The potential gains from buying barrels at the artificially low prices encourages companies to acquire as much pipeline capacity as possible, further increasing over-nominations.

Second, over-nominations can affect the allocation of capacity across shippers. As noted above, verifications are, in effect, limited to assessing shippers’ physical capabilities. Some participants in the NEB’s consultations were of the view that existing nomination and verification procedures tend to favour integrated producers and companies that own or have contracted capacity with storage and refining assets in Canada and the United States. By having access to large facilities upstream and downstream of export pipelines, these companies are better able to demonstrate that they have the physical capability to supply considerable volumes to, and remove considerable volumes from, pipelines. In the absence of rigorous verification, a shipper can leverage its investments in infrastructure to over-nominate up to its physical capabilities. Several market participants suggested that this increased ability to over-nominate may be unfair and may prevent pipelines from complying with common carrier requirements.Footnote 13

On the other hand, prevailing market conditions have different impacts on upstream producers and downstream refiners. While shippers that own refining and storage capacity currently have a greater ability to acquire pipeline capacity in current circumstances, these companies have faced high supply costs in other market conditions, which benefited producers.

During the NEB’s consultations, some market participants explained that there is no discrimination in the current nomination and verification practices, as shippers have been free to develop business strategies and make investment decisions in order to manage their risks and exposures. According to these industry participants, all shippers had an opportunity to prepare for the current apportionment environment by making investments that would help them acquire pipeline space, or by entering contracts with owners of storage and refineries. Small producers may lack the financial resources to make large investments or enter into long-term commitments.

Potential solutions to over-nominations

Under the existing nomination and verification procedures, the utilization of pipeline capacity is operationally efficient. There is broad agreement among industry participants that the four major export pipelines are full. Changes to the nomination or verification procedures would reallocate pipeline space among shippers, but would not increase utilization further. Changes could, however, reduce the number of apportioned barrels that are ultimately “pushed back” to producers.

The previous section of this report outlines potential issues with the existing verification procedures, including the lack of integrated oversight and transparency across different facilities in the crude oil supply chain. These issues relate not only to NEB-regulated pipelines, but also facilities, companies, and behaviours that extend beyond the NEB’s jurisdiction. For this reason, any improvements to existing verification procedures must be developed and coordinated across jurisdictions. They cannot be addressed by the NEB alone.

Verification-based solutions

Verification procedures are a complex, interjurisdictional issue.

There is scope to improve existing verification procedures. Such improvements could take a variety of different forms, ranging from minor adjustments to designing and establishing a new and integrated verification framework. This extends beyond the NEB’s oversight of federally-regulated pipelines.

As nomination verification is complex and cross-jurisdictional, there is significant risk of unintended consequences in making material changes to existing verification procedures without broad consultation with industry, governments, and regulatory bodies. Therefore, any material changes to the existing verification procedures are likely best developed in collaboration with industry participants and relevant governments or regulatory bodies.

Accordingly, if the Minister were to decide changes to existing verification procedures should be explored, an effective first step may be to have an interjurisdictional technical conference to discuss these changes. Participants in the technical conference should include: producers; marketers; operators of feeder pipelines, terminals, and large export pipelines; refiners; the COLC; other industry associations; relevant provincial governments and provincial regulators; Natural Resources Canada; and the NEB.

Potential topics for discussion at a technical conference could include, but are not limited to:

- The goals and objectives of verification procedures.

- The need for, and design of, uniform verification rules that could be applied across all or certain key facilities in the crude oil supply chain.

- The need to require all facilities to verify nominations on a regular basis.

- How to enforce compliance with verification rules.

- How to improve coordination and the flow of data between facilities that perform verifications.

- The identification and mitigation of any advantages or disadvantages inherent in the existing verification procedures.

During its consultations, NEB staff heard a number of different high-level suggestions from industry participants regarding improvements to verification procedures. The viability of these suggestions could be discussed at a technical conference. For example, the COLC has developed a proposal for enhanced verification guidelines that could be applied at all facilities upstream of export pipelines. Many industry participants indicated that the implementation of these guidelines would represent a significant improvement to existing verification procedures. This improvement would be based on the use of the guidelines being mandated for all facilities and compliance with the system being enforced. A technical conference could be used to discuss how to achieve universal use of the guidelines and effective oversight and enforcement.

Any solution should recognize that different industry participants will have opposing views on verification procedures throughout the supply chain. Nomination and verification procedures should not hinder shippers who currently have the flexibility to engage in trading activities to secure supplies, while at the same time ensuring that no company has a disproportionate advantage or disadvantage in acquiring pipeline capacity under the procedures. Any changes to nomination or verification procedures that involve revisions to NEB-regulated pipelines’ tariffs would require adjudication by the NEB.

Allocation-based solutions

Rather than using nomination and verification procedures, pipeline capacity could instead be allocated using alternative allocation methodologies, which are generally not favoured by industry.

The preceding section of this report discusses potential improvements to the industry’s verification procedures. In spite of the issues identified earlier in the report, Board staff heard that there is continued support among industry participants for the current pro rata apportionment system.

During its consultations with industry participants, NEB staff discussed different methodologies for allocating uncommitted pipeline capacity to shippers, including auctions. These alternative methodologies are generally not favoured. Alternative methodologies may offer some theoretical benefits, but in implementation carry many practical economic and technical risks. For example, an auction may better allocate uncommitted capacity to those shippers who value it most. However, an “all or nothing” pipeline capacity allocation methodology, such as an auction system, would increase uncertainty for shippers and refiners. This may disrupt contractual relationships between producers, marketers, and downstream buyers, and could also have impacts on the efficient operation of downstream facilities and markets.

Implementing alternative allocation methodologies would likely require changes to each NEB-regulated pipeline’s transportation tariffs. The NEB would need to adjudicate such changes.

F. Crude by rail

Markets

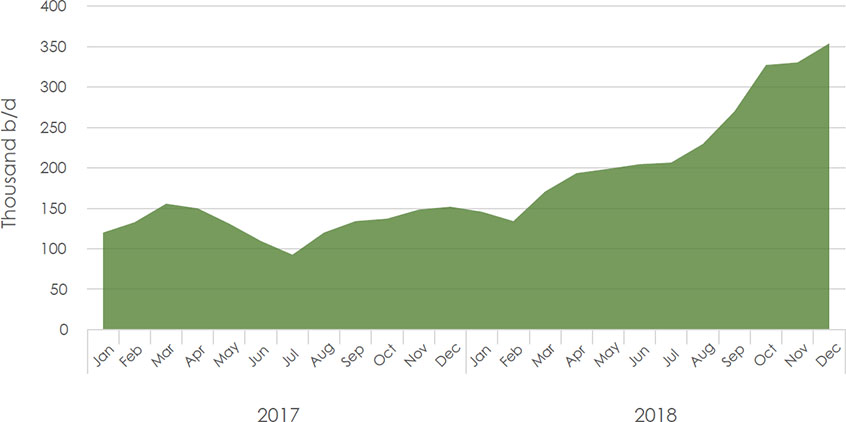

Although crude oil exports by rail increased throughout 2018, shipping crude by pipeline is generally preferred.

Exports reached 354 thousand b/d in December 2018. However, some producers have publicly announced a significant reduction in the volume of crude moved by rail in January.

Current rail infrastructure in Canada is operating at or near capacity, moving many commodities, of which crude oil is only a small fraction. The capacity to ship crude oil by rail is a function of many factors, including availability of tank cars, locomotives, crews, tracks, and the demand on the system to ship other goods.

Shipping crude oil by rail to major markets in the United States generally costs US$15-22 per barrel, compared to US$5-10 per barrel by pipeline. As such, shipping by pipeline is generally preferred. Significant volumes of crude oil generally only move by rail when there is insufficient pipeline capacity available and the WCS-WTI price differential is wide enough to justify the higher rail cost. Due to its dependence on prices, the demand for shipping crude by rail is unpredictable.Figure F.1: Crude exports by rail

Source: NEB

Description

This graph shows exports of crude oil by rail in thousand barrels per day from January 2017 until December 2018. Exports by rail averaged 120 Mb/d in January 2017 and reached a high of 354 Mb/d in December 2018.

Complexities of crude by rail

Shipping crude by rail requires coordination between multiple parties.

Unit trains versus manifest trains

Unit trains move only one product directly between two locations. They also benefit from reduced turn-around times and are the most efficient way to move crude by rail. This makes them more economic at a narrower differential than manifest trains, which carry crude oil on individual cars, along with other cars transporting different cargoes. This adds time as the trains are required to stop at multiple destinations for loading and unloading. Though manifest trains are not as efficient as unit trains and cost more, they may be a more viable option for smaller or infrequent shipments.

The preferred method of transporting crude by rail is via the use of unit trains. A single unit train consists of approximately three to four locomotives moving 80 to 100 tank cars from one loading facility to a single destination. In order to ship crude oil by rail, a company must have the ability to transport crude into a rail loading facility, the rail cars to carry the crude, arrangements with a rail carrier who owns the tracks, and an agreement with a downstream refinery or terminal with the necessary rail unloading infrastructure.

Bringing a new unit train operation into service can take a rail carrier between 12 and 24 months. Recruiting and training crews along the proposed route, acquiring locomotives, and in some cases building additional sidings along the track to accommodate the increased rail traffic may all be required. There are long wait times for equipment and unpredictable demand for crude by rail service. Additionally, there is significant uncertainty regarding the timing of new pipeline infrastructure. As a result, investing in moving more crude by rail comes with considerable financial risk.

Potential solutions

Significant increases in crude by rail would only be possible in the medium to long term.

In Canada, rail carriers’ tracks tend to operate at capacity, particularly during grain harvest season. Therefore, a long-term investment in building new tracks would be necessary in order to significantly increase year-round crude by rail capacity. This would be a multi-year construction process, involving at least one to two years of permitting and regulatory processes. Furthermore, limited land may be available, especially in larger urban centres.

Investment in new rail cars, locomotives, or crews, by industry or governments, could take up to 1-2 years to come into service due to the lead times required to build equipment and recruit crews.

It is important to note that regardless of whether the capacity to ship crude by rail were increased, the price differential will be the primary factor that determines how much crude actually moves by rail. The unpredictability of Canadian crude differentials means that any investments in crude by rail infrastructure may come with considerable risk for Canadian producers as they are price takers. However, governments may have different priorities than private investors, such as increasing market diversification, employment, and government revenues.

G. Medium- to long-term solutions

Predictable timelines and clear policies help market participants make decisions.

Investment decisions are harder to make when policies are unclear, or outcomes and timelines for processes and projects relating to oil transportation infrastructure are unknown. This includes decisions on capital investment for new production, and decisions on how oil is marketed and transported. Greater certainty regarding proposed new pipeline capacity would help market participants predict when and how much pipeline capacity would come on stream, which would in turn allow them to arrange for rail contracts in the interim.

Providing more clarity on the expected completion and commissioning dates of proposed pipeline systems can be a near-term objective. However, some clarity may be difficult to provide, especially for systems which are subject to complex and multi-faceted regulatory processes.

In the absence of new pipeline capacity, some large infrastructure changes or additions could be considered. Several medium- to long-term options are described in this section. However, these changes or additions would be expensive and time consuming, would require regulatory approvals, and may become uneconomic if and when new pipeline capacity comes online.

Better market data could help market participants and policy makers make decisions in the near term about investments and actions in the medium to long term.

Decisions about investments and policy are based on information available at that time. Better, public market data could help market participants and policy makers make more-informed decisions. This includes decisions made in the near term about additional capacity that could come online in the medium to long term. Better market data could also help level the playing field between smaller market participants and larger market participants in making decisions about the medium to long term.

As mentioned earlier in the report, additional public data would be beneficial. In addition to this, it may be beneficial to collect and share data with limited groups at relevant times even if that data may not be made available to the public. For example, more confidential data could be shared with regulators and other government agencies.

Shipping undiluted bitumen

By shipping undiluted bitumen in rail cars, the volume of bitumen exported by rail can be increased.

If undiluted bitumen could be shipped by rail, the volume of bitumen that could be exported would increase by anywhere from 43% to 100%, depending on how much it would otherwise need to be diluted.Footnote 14 Undiluted bitumen is not classified as a dangerous good in the railway system. As a result, shippers can use a greater variety of rail cars.

However, rail loading facilities would need to be constructed near bitumen production sites or diluent recovery units would need to be built to remove diluent in diluted bitumen that was already shipped to Edmonton or Hardisty by pipeline. Downstream, refineries would need to build facilities to receive undiluted bitumen. This may include building heating units to remove the bitumen from the rail cars, as well as units to re‑dilute/blend the bitumen before processing it in the refinery. Some proposals for shipping raw bitumen involve creating bitumen pellets, bitumen balls, or “bitumen in a bag”.

Overall, the investment needed would be significant, and the required infrastructure may take years to build.

Additional upgrading to reduce diluent volume

More upgrading of bitumen to a higher quality product could reduce the volume of diluent needed and open up space on existing pipelines.

Canada exported about 2 million b/d of diluted bitumen in 2018. Fully upgrading more raw bitumen into synthetic crude oil (SCO, a high-quality light oil equivalent)Footnote 15, or partially upgrading more raw bitumen into heavy or medium sour oil, would reduce the need for diluent and free up space in existing pipelines.

Full and partial upgraders are significant investments and require years to permit and build. Currently, none of the proposed partial-upgrading technologies are operating commercially. One proponent indicates they may have a commercial, partial-upgrading pilot running by the end of 2022, costing around $1 billion and upgrading 45 thousand b/d of bitumen. The Government of Alberta recently awarded grants and loans to a proposed 77.5 thousand b/d partial upgrading project near Edmonton.Footnote 16

One advantage partial upgraders have over full upgraders is that partial upgraders would produce heavy to medium sour oils, which are sought after by refineries in the United States currently processing Canadian heavy oil. Additional SCO, on the other hand, would compete against growing light oil production in the United States. Upgrading, whether full or partial, is likely to be a better option than fully refining additional oil in Alberta, where refined petroleum markets are already adequately supplied.

If more pipeline space is eventually available, partial upgraders could sit idle if they are more expensive to operate than simply diluting bitumen. Governments may choose to take on this kind of investment risk to achieve policy objectives.

Reversing diluent-import pipelines to export crude oil

Canada currently imports a significant amount of diluent through two pipelines. If these were reversed, Canada could export more crude oil.

Importantly, the hydrocarbons used to dilute bitumen must be acquired. Western Canada produces a significant amount of condensate and pentanes plus, which are used as diluent. However, western Canada does not produce enough to meet demand and currently 215 thousand b/d of diluent is imported on the Enbridge’s Southern Lights and Kinder Morgan’s Cochin pipelines.

If the companies owning one or both of these pipelines wanted to reverse them, these pipelines could be used to export crude oil from western Canada to Illinois, a market which already consumes a significant amount of Canadian crude oil. The reversal would take over a year of work, not including the time required for regulatory approvals.

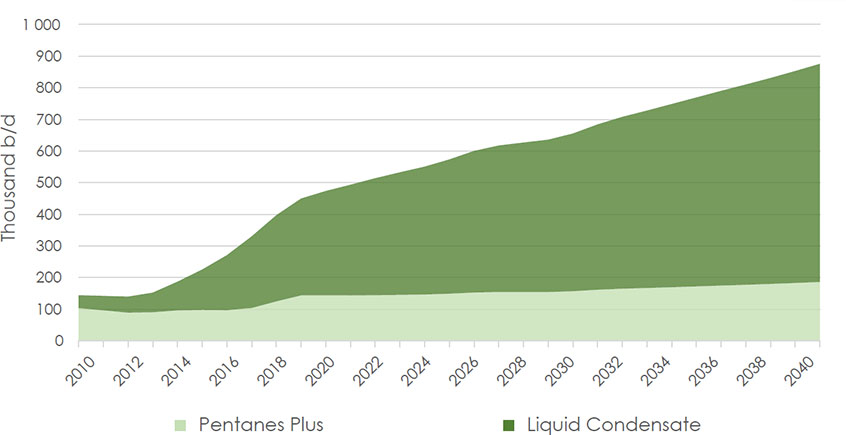

However, this would impact western Canada’s diluent market, significantly raising prices and operating costs for oil sands producers. Domestic production of condensate and pentanes plus grew over 100 thousand b/d per year since 2017 because of development of liquids-rich natural gas. From this perspective, one year of growth is enough to replace most of Southern Lights’ throughput and two years of production growth would be enough to replace most diluent imported on both pipelines. The graph shows projected supply of condensate and pentanes plus in western Canada from Canada’s Energy Future 2018: Energy Supply and Demand Projections to 2040. However, natural gas production partly depends on natural gas prices and the extra diluent supply may not materialize as projected.

Figure G.1: Western Canada condensate and pentanes plus supply

Source: NEB

Description

This graph shows western Canadian condensate and pentanes plus production from 2010 to 2040. Total production was 397 thousand barrels per day in 2018. This increases to 573 thousand barrels per day in 2025, and 876 thousand barrels per day in 2040.

There are also several Canadian and U.S. regulatory approvals that would be required to reverse a pipeline with associated time requirements and policy impacts.

H. Considerations

When markets or rules change, market participants need to adjust accordingly, sometimes in unpredicted ways.

This report identifies a number of concerns raised by participants in the western Canadian crude oil market, along with possible paths forward to address these concerns. While considering the implications of any government action, it is important to note that not all outcomes can be predicted. Market participants build business models and make investment decisions based on expected market conditions (such as supply, demand, and infrastructure) and market rules (such as policies, legislation, regulations, and the rules and regulations set out in pipeline and rail tariffs). When there are changes to market rules or conditions, companies may adapt in ways that are difficult to foresee.

Accordingly, any actions need to be carefully considered. Broad consultation across industry stakeholders, regulators and governments at all levels would be required. Many of the options would also require regulatory changes or adjudication by a regulatory body such as the NEB following a regulatory process.

- Date modified: