Market Snapshot: Canadian Exploration & Production companies raised over $9 billion from corporate bonds during 2020

Connect/Contact Us

Please send comments, questions, or suggestions for Market Snapshot topics to snapshots@cer-rec.gc.ca

Release date: 2021-07-14

Canadian oil and gas exploration and production (E&P) companies’ cash flow from operationsDefinition* was negatively impacted during 2020 largely because of the decline in oil demand and prices due to the effects of the COVID-19 pandemic.Footnote 1 The breakdown in negotiations related to production cuts between OPEC+Footnote 2 countries in the spring of 2020 also negatively impacted oil prices and companies’ cash flows. Canadian E&P companies’ cash flow from operations was about $29.3 billion lower in 2020 compared to 2019.

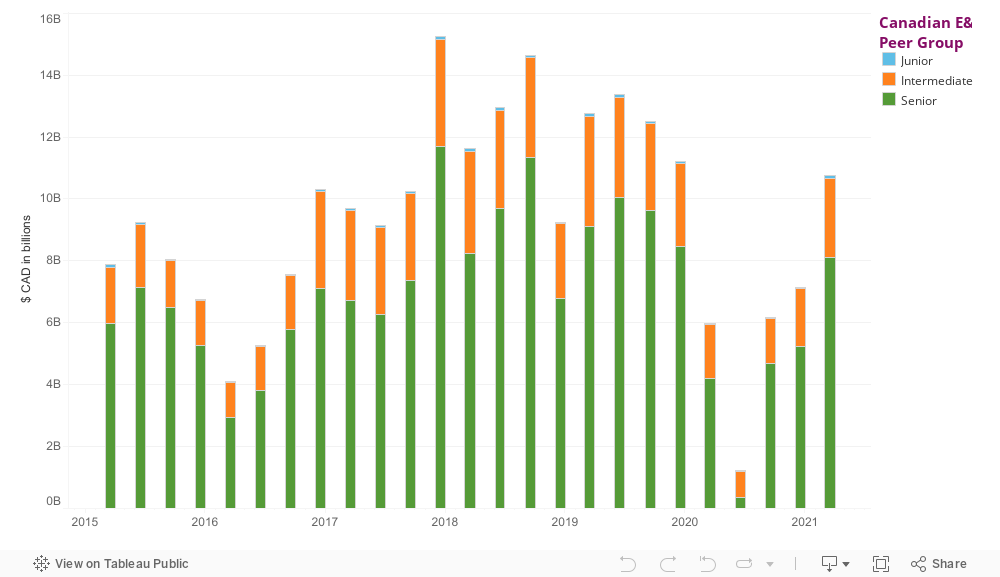

Figure 1: Total Cash from Operations by Canadian E&P Companies 2015-2021 Q1

Source and Description

Source: CanOils dataset of companies with publicly available financial statements

Description: This stacked column chart shows total cash from operations (CFO) of Canadian E&P companies by peer group: senior, intermediate, junior from Q1 2015 to 2021. Canadian E&P companies’ aggregate CFO was $29.3 billion lower in 2020 compared to 2019. Over the five year period, all Canadian E&P peer groups reported the lowest total CFO during 2020 Q2, with total CFO in Q2 2020 $4.7 billion lower than the previous quarter and over $12 billion lower than 2019 Q2. Canadian E&P companies’ CFO recovered slightly in the second half of 2020, but was still $4 billion lower by the end of Q4 2020 compared to Q4 2019. By Q1 2021, E&P companies’ CFO was $4.8 billion higher compared to 2020 Q1.

Due to the substantial reduction in cash flow during 2020, E&P companies significantly increased their debt during this period in order to sustain their operations.Footnote 3 Particularly, Canadian E&P companies relied more heavily on financing from the capital marketsDefinition* during the year and collectively raised over $9.7 billion from corporate bond issuances during 2020 (Figure 2).

However, the majority of this $9.7 billion was issued by four senior E&PDefinition* companies. Senior E&P companies received roughly 75% of this $9.7 billion, raising $7.3 billion from new corporate bond issues throughout 2020.Footnote 4 Whereas intermediateDefinition* and juniorDefinition* companies raised only $2.3 billion in proceeds from debt issued via the capital markets over the same period.

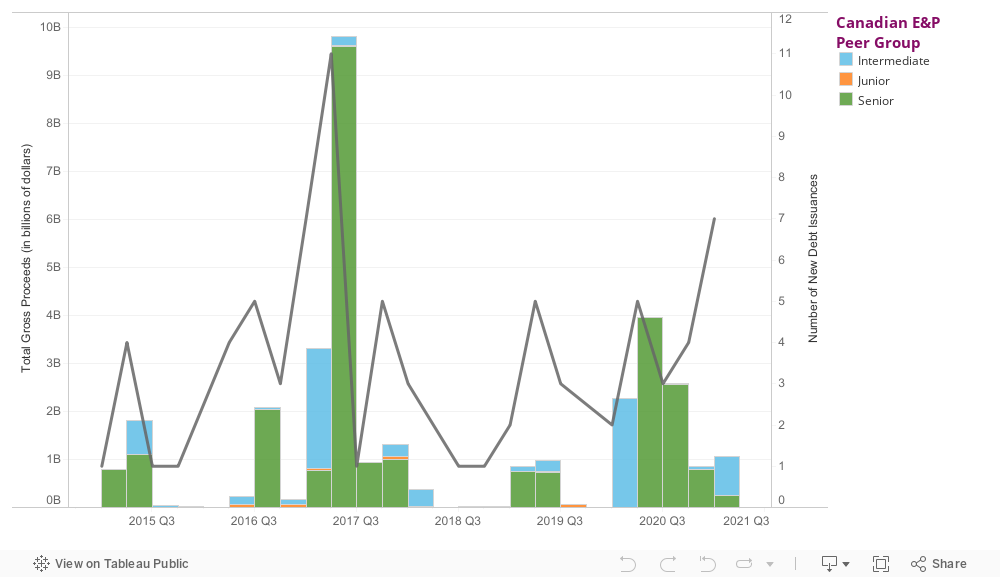

Figure 2. Total New Debt Issued by Canadian E&P Companies 2015-2021 Q1

Source and Description

Source: CanOils dataset of companies with publicly available financial statements

Description: This combination line and bar chart shows the total number of new corporate bonds issued by Canadian E&P companies as well as the total gross proceeds of the new issuances measured in billions of Canadian dollars from Q1 2015 to 2021. The total value of new debt issued by Canadian E&P companies was much higher in 2020 ($9.7 billion) compared to 2019 ($1.9 billion), but still less than in 2017 ($15.4 billion).

Why a company may issue debt in the capital markets versus getting a bank loan:

When a company needs to borrow money, it has two options: they can either get financing from a bankDefinition*, or the company can issue corporate bonds in the capital markets. Debt raised in the capital markets is referred to as a “debt issue”. Debt issue is the issuance of corporate bonds by a company in need of capital to fund new or existing projects. A company may choose to issue corporate bonds rather than go to a bank for a loan because bank loans often have more restrictions with how the funds are used. For this reason, raising new debt via the capital markets may be the preferred method for companies that need to raise funds to finance a new project, or to sustain their operations.Footnote 5 Canadian E&P companies raised more than $9.77 billion from new debt issued in the capital markets during 2020. (Figure 2).

During 2020, senior producers relied more heavily on obtaining new financing through issuing corporate bonds via the capital markets over getting loans from a bank and were able to issue new corporate bonds at significantly lower interest rates compared to their intermediate and junior peers. By contrast, junior E&P companies did not raise a material amount of funds from the capital markets during 2020 for financing, and unlike their larger peers, junior producers actually reduced their existing long-term debtFootnote 6 by $1.9 billion during 2020 compared to 2019. Instead, junior producers relied more on shorter-term bank loans and credit facilities throughout the year and by Q4 2020, junior E&P’s paid back a lot of this short-term debt as well (Figure 3).

The junior companies’ greater reliance on short-term loans from banks, combined with the substantial repayment to lenders throughout the year highlights that junior companies likely faced greater challenges when trying to raise additional funds from investors in the capital markets compared to their larger peers who were able to issue billions of dollars in new financing at lower interest rates.

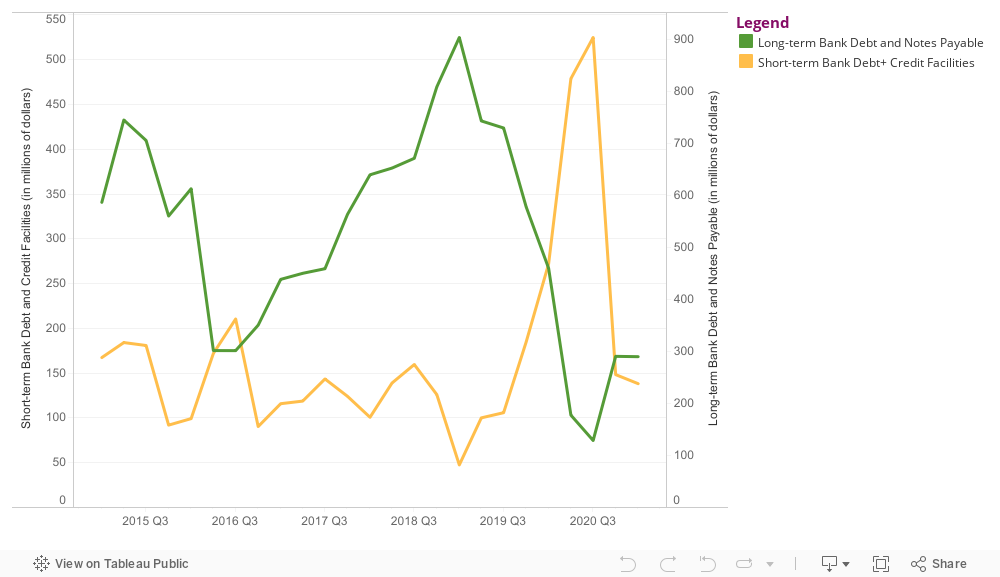

Figure 3. Total Long-term and Short-term Bank Debt reported by Junior Companies

Source and Description

Source: CanOils data of companies with publicly available financial statements

Description: This line chart shows junior E&P companies long-term debt (including long-term bank debt and notes payable) and short-term debt (including short term bank debt and revolving credit facilities) from Q1 2015 to 2021. Junior E&P companies’ use of long-term debt has been on a notable decline since the start of 2019, while their use of shorter-term bank debt and credit facilities increased significantly over the same period.

Unlike their junior peers, senior E&P companies’ total debtDefinition* increased by $11 billion in 2020 compared to 2019, and intermediate producers’ total debt grew by $2 billion over the same period. At the same time, intermediate and senior producers’ shareholders’ equityFootnote 7 declined by a combined $173 billion during 2020 compared to 2019. The substantial loss in shareholders’ equity was driven by the large net losses reported by both intermediate and senior producers during 2020. These losses were largely a result of lower production and lower prices which negatively affected their upstream earnings. The combination of the substantial loss in their shareholders’ equity, as well as their large increase in debt drove senior and intermediate E&P companies’ debt-to-capitalDefinition* ratios higher when compared to any other period throughout 2015-2020. (Figure 4).

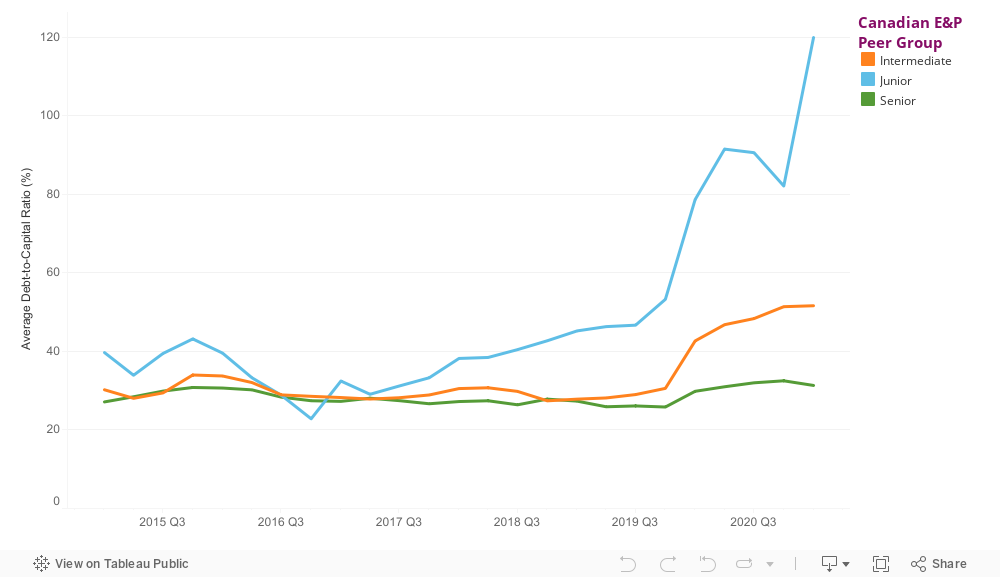

Figure 4. Debt-to-Capital Ratios of Canadian E&P Companies from Q1 2015-2021

Source and Description

Source: CanOils dataset of companies with publicly available financial statements

Description: This line graph shows the debt-to-capital ratios of Canadian E&P companies from Q1 of 2015 to 2021. Senior E&P companies debt-to-capital ratio averaged 28% from 2015 to 2019 and rose to 31% in 2020 on average. Intermediate E&P companies’ debt-to-capital ratio averaged 29% from 2015 to 2019 and rose to 47% in 2020 on average. Junior E&P companies’ debt-to-capital ratio averaged 37% from 2015 to 2019 and rose to 86% in 2020 on average.

Despite reducing the amount of debt on their balance sheets, junior E&P companies’ capital structure was the most negatively impacted relative to their larger peers, with their debt-to-capital ratio rising to a high of 119%Footnote 8 by 2021 Q1. A higher debt-to-capital ratio means that the company is riskier all else being equal. This is because when a company is funded by more debt relative to equity, all else being equal, the company has a greater risk of defaulting on their debt.

The rise in the junior’s debt-to-capital ratio was mainly because of the large net lossesFootnote 9 recorded by many junior companies during 2020, which led to a material reduction in their shareholders’ equity.Footnote 10 This significant loss in the junior E&P’s shareholders’ equity more than offset their reduction in debt during the year and led to the rise in the juniors’ overall debt-to-capital ratio during 2020.

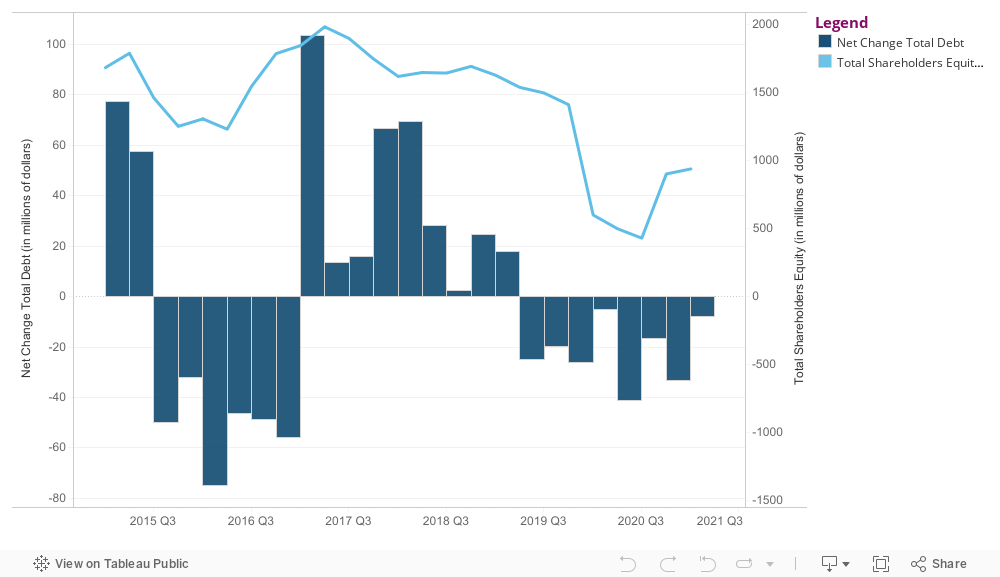

Figure 5. Net Debt and Shareholders’ Equity of Junior E&P Companies

Source and Description

Source: CanOils data of companies with publicly available financial statements

Description: This combination column and line chart shows Canadian junior E&P companies change in total net debt and shareholders’ equity from Q1 2015 to 2020. During 2020, junior E&P companies have on net, paid back more debt than they have issued. Shareholders’ equity has been on a downward trend since 2017 for junior E&P companies.

Overall, in 2020 the COVID-19 pandemic resulted in large reductions in cash from operations and shareholders’ equity for many E&P companies due to the unprecedented declines in production volumes and oil prices. The decline in companies’ shareholders’ equity as a result of substantial net losses was the biggest contributor to the rise in Canadian E&P companies’ debt-to-capital ratios during this period.

Larger Canadian E&P companies were able to access the capital markets and issued a substantial amount of new corporate bonds at relatively low interest rates to help sustain their operations throughout 2020. Conversely, junior E&P companies did not issue any material amount of bonds from the capital markets during 2020, and instead relied on shorter-term bank loans to manage through the deteriorating market conditions.

- Date modified: