Market Snapshot: Investment in Canada’s oil and gas sector declined from 2014 high

Release date: 2018-08-01

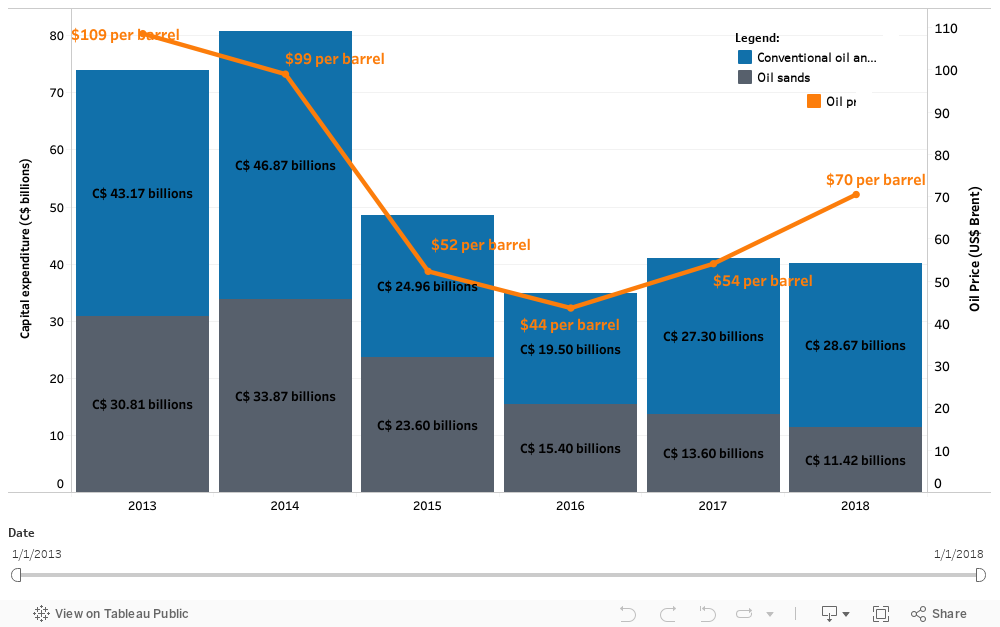

Investment in Canada’s oil and gas sector declined in the last several years from a high in 2014.

Brent crude oil averaged US$99 per barrel (bbl) in 2014 when, according to an industry survey by Oil and Gas Journal (OGJ), capital spending on Canadian oil and gas reached a peak at C$80.7 billion. When oil prices dropped to US$44/bbl in 2016, capital spending declined as well, by 57% to C$34.9 billion. The average 2018 year-to-date price of benchmark crude Brent is US$70/bbl. This is more than 60% higher than 2016 lows; the OGJ expects 2018 spending to be C$40.1 billion, or 15% higher than 2016.

Oil and Gas Spending in Canada

Source and Description

Source: Oil and Gas Journal (OGJ), Brent Oil Price – Energy Information Administration

Description: The chart shows capital investment in Canadian oil and gas and the price of Brent crude oil in U.S. dollars. The stacked column chart shows investment in conventional oil and gas in blue and investment in the oil sands in orange. The yellow line shows the per barrel price of Brent Crude. All data is for the years 2013 to 2018. In 2013 and 2014, capital investment rose, peaking in 2014 at over C$80 billion and declining in 2015 and 2016 before a slight recovery in 2017 and 2018 to around C$40 billion. The price of Brent crude in 2013 was well above US$100 per barrel, declining slightly in 2014, before a steep fall in 2015 to around US$52 per barrel. Prices have recovered since 2016, and year-to-date are around US$70 per barrel.

Spending on conventional oil and gas (including tight oil and tight gas) in western Canada has been increasing from 2016 lows. This is partly because gas producers are increasingly targeting liquids-rich plays that produce condensate, which sells at a higher price than oil in western Canada.

Investment in the oil sands however, continues to decline, despite a rise in global oil prices since 2016. OGJ expects investment in the oil sands to be C$11.4 billion in 2018, or two thirds lower than 2014.

There are a number of factors contributing to reduced investment in Canada’s oil sands:

-

Production continues to grow in recent years, a result of investment decisions made before the price downturn. However, pipeline capacity has remained essentially constant since 2016, contributing to a widening of the price differential between Canada’s heavy oil and North American’s light crude benchmark. When the price differential is high, Canadian producers receive comparatively less revenues for their production. This also leads to a growing amount of oil needing to be shipped out of Canada by rail cars.

- The production increases are because of a significant number of new and expanded oil sands projects coming online in recent years. Typically, periods of increased investments are followed by a period of lower investments as companies redirect cash flow to their investors.

- While global oil prices have increased over the last two years, uncertainties persist. This leads investors to favour shorter-term investments. Tight oil, in Canada and the U.S., requires much less up front capital to develop and achieves returns on investment much quicker than a typical oil sands project.

- Date modified: