ARCHIVED – Canada’s Energy Future 2013 - Energy Supply and Demand Projections to 2035 - An Energy Market Assessment

This page has been archived on the Web

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please contact us to request a format other than those available.

Feedback

For further information about the report Canada’s Energy Future 2013 - Energy Supply and Demand Projections to 2035, please email us at energyfutures@cer-rec.gc.ca.

November 2013

Copyright/Permission to Reproduce

ISSN 2292-1710

Table Of Contents

- List of Figures

- List of Tables

- List of Acronyms and Abbreviations

- List of Units

- Foreword

- Executive Summary

- Chapter 1: Introduction

- Chapter 2: Energy Context

- Chapter 3: Key Drivers

- Chapter 4: Energy Demand Outlook

- Chapter 5: Crude Oil Outlook

- Chapter 6: Natural Gas Outlook

- Chapter 7: Natural Gas Liquids Outlook

- Chapter 8: Electricity Outlook

- Chapter 9: Coal Outlook

- Chapter 10: Conclusion

- Glossary

- Conversion Tables

- Endnotes

- Appendices

List of Figures

- ES.1 Energy Production in Canada, on an Energy Equivalent Basis

- ES.2 Energy Demand by Sector: Historic and Projected Growth

- 1.1 Price Projections to 2035, All Cases

- 2.1 Combined Canada and U.S. Marketable Natural Gas Production by Type

- 2.2 Canadian Tight Oil Production

- 2.3 U.S. Tight Oil Production

- 2.4 U.S. Vehicle Kilometres Travelled and Transportation Petroleum Consumption

- 2.5 Benchmark Oil Prices

- 2.6 Benchmark Oil Prices and Price Differentials

- 2.7 Railway Car Loading, Fuel Oils and Crude Petroleum, Western Canada

- 2.8 B.C., Alberta and Saskatchewan Combined Production and Consumption

- 2.9 Annual Canadian Electricity Exports, Imports and Export Revenue

- 3.1 WTI Crude Oil Price at Cushing, Oklahoma, All Cases

- 3.2 Henry Hub Natural Gas Price at Louisiana, All Cases

- 3.3 Annual GDP Growth, Reference Case

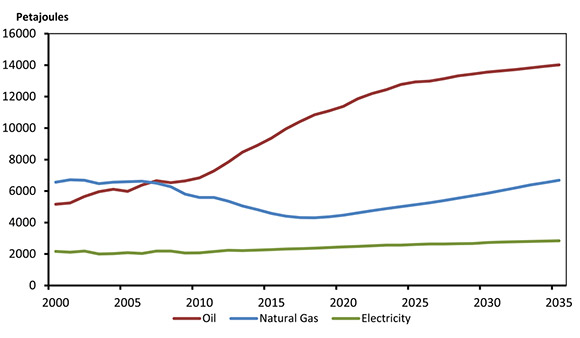

- 4.1 End-Use Energy Demand by Sector, Reference Case

- 4.2 Residential Energy Demand, Reference Case

- 4.3 Commercial Energy Demand, Reference Case

- 4.4 Industrial Energy Demand, Reference Case

- 4.5 Transportation Energy Demand by Travel Type, Reference Case

- 4.6 Transportation Energy Demand by Fuel, Reference Case

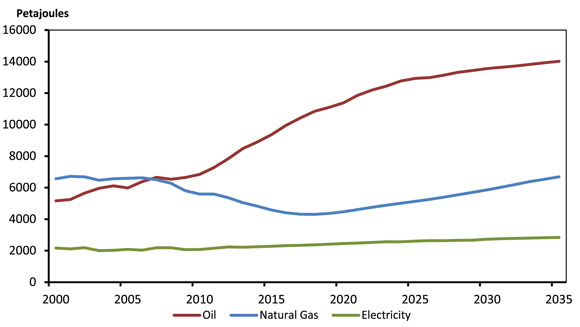

- 4.7 Share of Fuel in Primary Energy Demand, Reference Case

- 4.8 Primary Natural Gas Demand, Reference Case

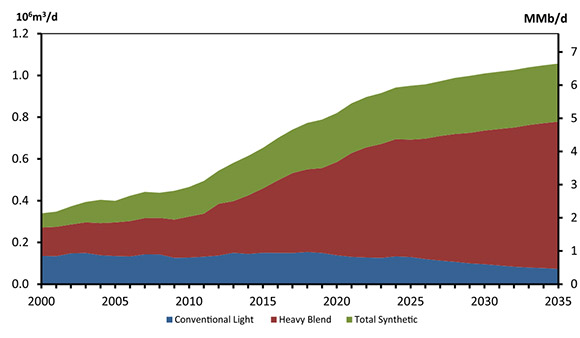

- 5.1 Total Canadian Crude Oil and Equivalent Production, Reference Case

- 5.2 Oil Sands Production and Projection Comparison, Reference Case

- 5.3 Purchased Natural Gas for Oil Sands Extraction and Upgrading, Reference Case

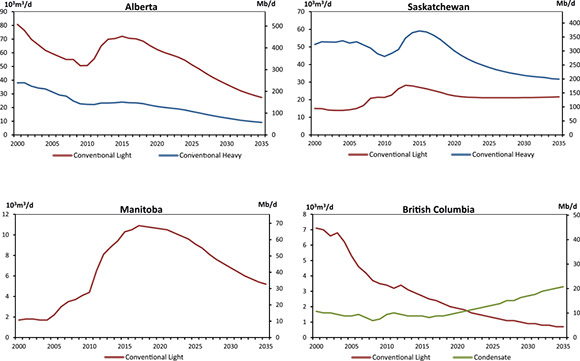

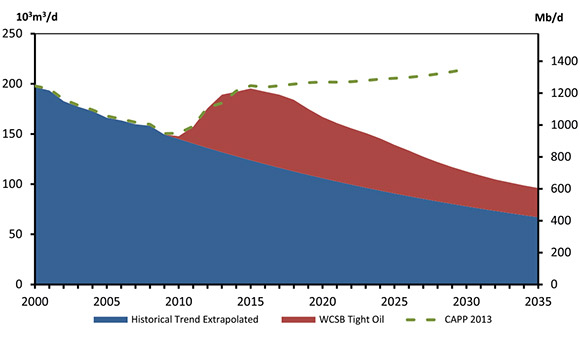

- 5.4 WCSB Conventional Oil Production, Reference Case

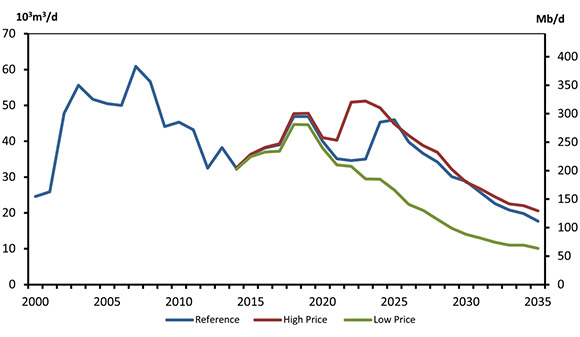

- 5.5 WCSB Incremental Tight Oil Production, Reference Case

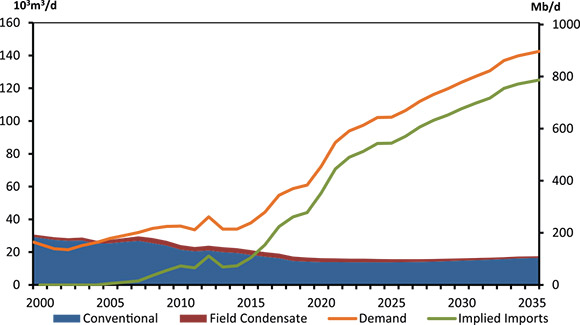

- 5.6 Eastern Canada Oil Production, All Cases

- 5.7 Total Canada Oil Production, All Cases

- 5.8 Net Available Oil Supply, Reference Case

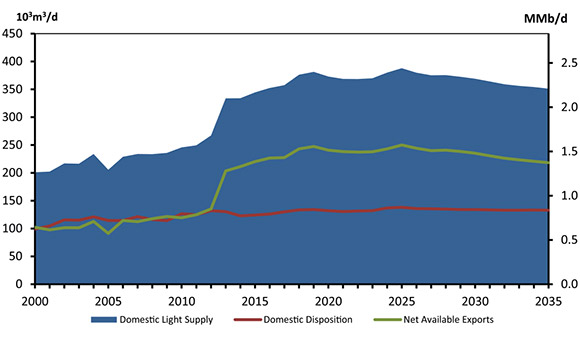

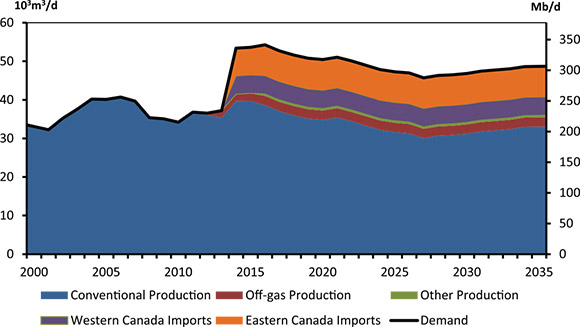

- 5.9 Supply and Demand Balance, Light Crude Oil, Reference Case

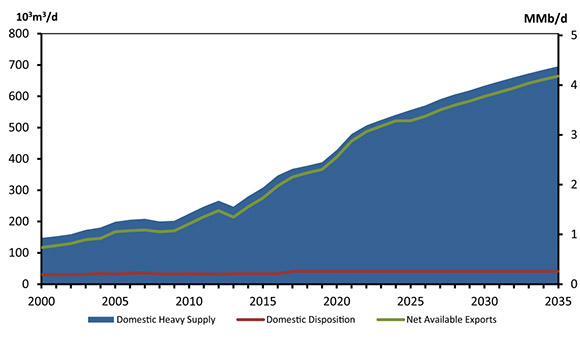

- 5.10 Supply and Demand Balance, Heavy Crude Oil, Reference Case

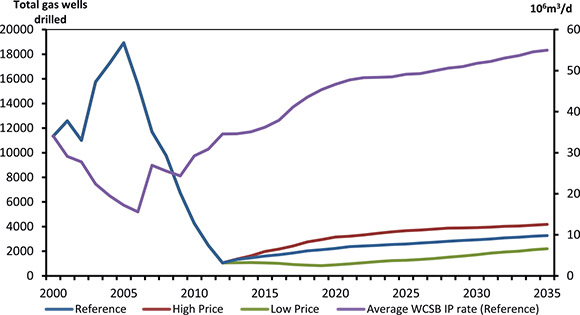

- 6.1 Natural Gas Wells Drilled, All Cases, and Average IP Rate

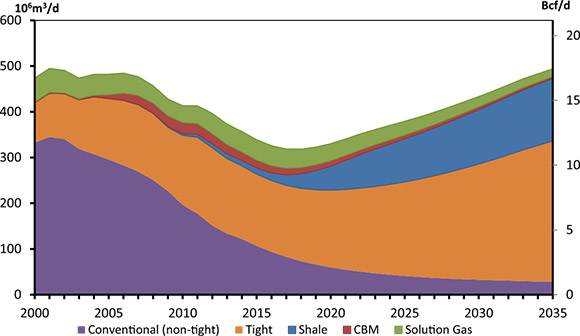

- 6.2 Natural Gas Production by Type, Reference Case

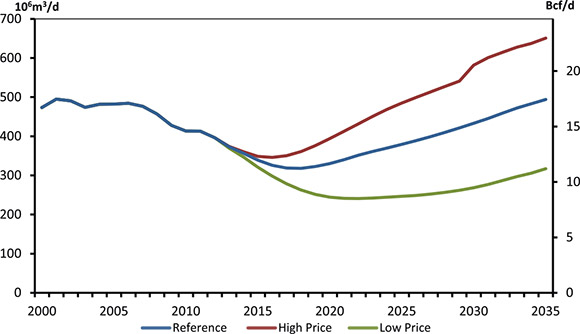

- 6.3 Total Canadian Marketable Gas Production, All Cases

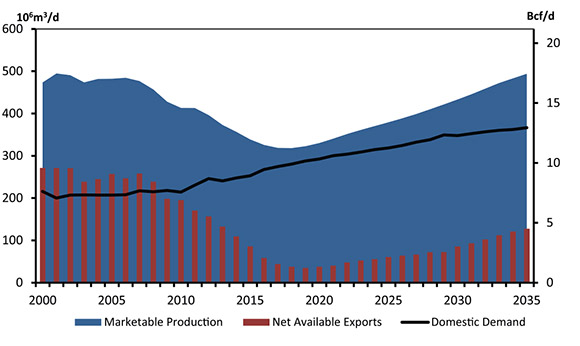

- 6.4 Canadian Net Natural Gas Available for Export, Reference Case

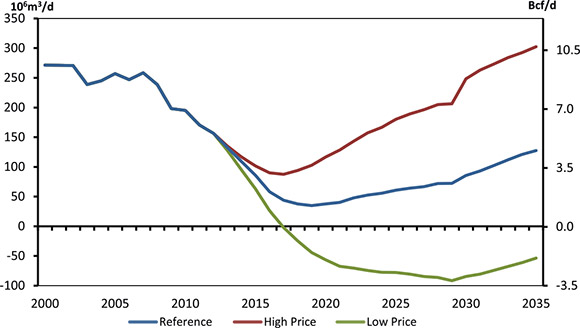

- 6.5 Canadian Net Natural Gas Exports, by Case

- 7.1 Natural Gas Liquids Production, Reference Case

- 7.2 Pentanes Plus Supply and Demand, Reference Case

- 7.3 WCSB Ethane Availability in Raw Gas and Ethane Production, Reference Case

- 7.4 Ethane Supply and Demand Balance, Reference Case

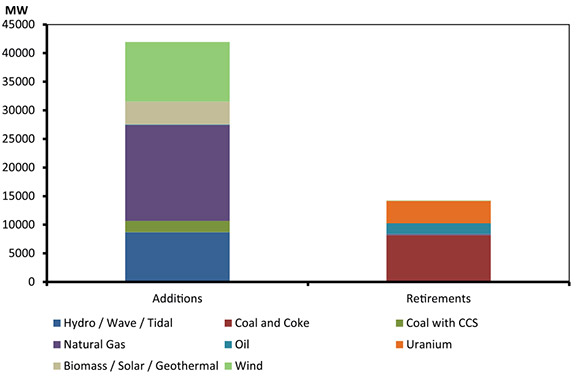

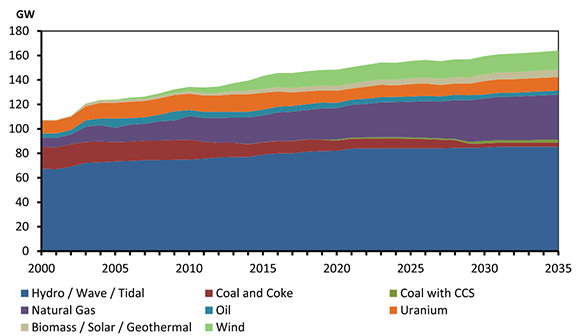

- 8.1 Capacity Additions and Retirements by 2035, Reference Case

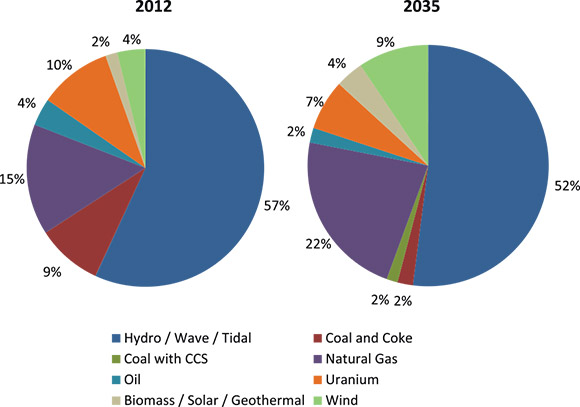

- 8.2 Capacity Mix by Primary Fuel, 2012 and 2035, Reference Case

- 8.3 Capacity by Primary Fuel, Reference Case

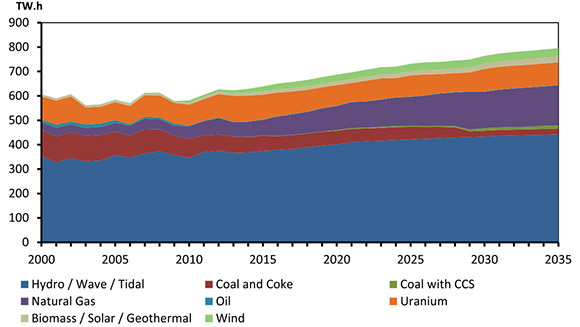

- 8.4 Generation by Fuel, Reference Case

- 8.5 Electricity Net Available for Export and Interprovincial Interchange, Reference Case

- 9.1 Canadian Coal Production and Disposition, 2010, 2020 and 2035, Reference Case

- 10.1 Production of Crude Oil, Natural Gas and Electricity, Reference Case

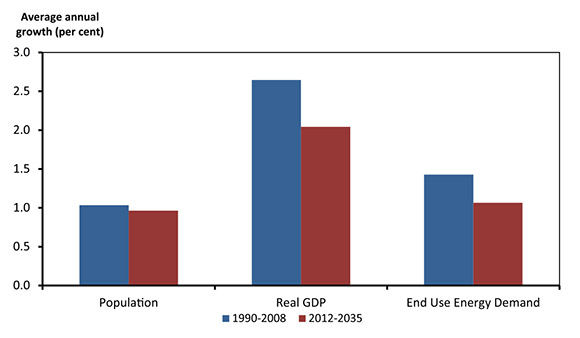

- 10.2 Comparison of Historical and Projected Growth Rates of Population, Real GDP, and End-use Energy Demand, Reference Case

List of Tables

- 2.1 Long-term Natural Gas Export Licences and Applications Under Review as of 1 October 2013

- 5.1 Remaining Ultimate Potential and Established Reserves, as of 31 December 2012

- 5.2 Estimated Initial Capital Expenditure (CAPEX) and Threshold Prices for New Oil Sands Projects

- 6.1 Remaining Marketable Natural Gas Resources, as of 31 December 2012

List of Acronyms and Abbreviations

List of Units

Foreword

The National Energy Board (NEB or Board) is an independent federal regulator whose purpose is to promote safety and security, environmental protection and efficient infrastructure and markets in the Canadian public interest[1] within the mandate set by Parliament for the regulation of pipelines, energy development, and trade.

The Board’s main responsibilities include regulating the construction and operation of interprovincial and international oil and natural gas pipelines, international power lines, and designated interprovincial power lines. Furthermore, the Board regulates the tolls and tariffs for the pipelines under its jurisdiction. With respect to the specific energy commodities, the Board regulates the export of natural gas, oil, natural gas liquids (NGLs) and electricity, and the import of natural gas. Additionally, the Board regulates oil and natural gas exploration and development on frontier lands and offshore areas not covered by provincial or federal management agreements.

For oil and natural gas exports, the Board’s role is to evaluate whether the oil and natural gas proposed to be exported is surplus to reasonably foreseeable Canadian requirements, having regard to the trends in the discovery of oil or gas in Canada.[2] The Board monitors energy markets, and provides its view of Canadian energy requirements and trends in discovery of oil and natural gas to support its responsibilities under Part VI of the National Energy Board Act (the NEB Act). The Board periodically publishes assessments of Canadian energy supply, demand and markets in support of its ongoing market monitoring. These assessments address various aspects of energy markets in Canada. This report, Canada’s Energy Future 2013: Energy Supply and Demand Projections to 2035 is one such assessment that projects Canadian energy supply and demand trends out to 2035.

While preparing this report, in addition to conducting its own quantitative analysis, the NEB held a series of informal meetings and discussions with industry, academia, other government agencies and departments, non-governmental organizations (NGOs), energy experts, and interested stakeholders. The NEB appreciates the information and comments provided and would like to thank all participants for their time and expertise.

If a party wishes to rely on material from this report in any regulatory proceeding before the NEB, it may submit the material, just as it may submit any public document. Under these circumstances, the submitting party in effect adopts the material and that party could be required to answer questions pertaining to the material.

This report does not provide an indication about whether any application will be approved or not. The Board will decide on specific applications based on the material in evidence before it at that time.

Comments or questions on this report can be directed to:

energyfutures@cer-rec.gc.ca.

Executive Summary

Canada’s Energy Future 2013: Energy Supply and Demand Projections to 2035 (EF 2013) reports enough energy supplies will be available to meet Canada’s growing energy needs for the foreseeable future. Over the next 20 years, the NEB projects energy production levels increasingly greater than domestic needs, resulting in growing amounts of energy available for export.

Total Canadian production grows substantially over the projection period.

Canada has vast energy resources. The oil and natural gas resource base is large enough to meet Canadian needs for many generations, and abundant hydroelectric resources account for the majority of the electricity mix. Considering this resource base, as well as the projected commodity prices and economic drivers, EF 2013 projects total Canadian energy production to grow substantially in the future.

Oil production leads this growth, with 2035 production reaching 928 10³m³/d (5.8 MMb/d), or nearly 75 per cent higher than in 2012. In situ oil sands production makes up the majority of the increase. Natural gas production increases 25 per cent above current levels by 2035, led by higher levels of tight and shale gas development.

Canadian electricity supply also steadily increases over the projection period. Natural gas-fired power generation capacity increases substantially. Coal-fired generation capacity declines, largely a result of federal and provincial regulations. Non-hydro renewable capacity doubles its share of Canada’s electricity capacity mix. Total electricity generation increases 27 per cent over the projection period.

Figure ES.1 - Energy Production in Canada, on an Energy Equivalent Basis

Total Canadian energy use grows moderately.

EF 2013 projects that total energy consumed by Canadians will continue to grow, but at a slower rate than in the past.

Hydrocarbons continue to be the main source of energy to heat homes and businesses, transport people and goods, and many other functions that are integral to Canadians’ standard of living. Canadian demand for oil and natural gas increases by 28 per cent over the projection period. Emerging fuels and technologies, such as solar hot water heating and electric vehicles, continue to gain market share.

Figure ES.2 - Energy Demand by Sector: Historic and Projected Growth

Canadians use energy more efficiently.

By 2035, the energy used per unit of economic output is projected to be 20 per cent lower than in 2012, due to improvements in energy efficiency. In a reversal of the long-term trend, passenger transportation energy use declines over the projection, largely due to new passenger vehicle emission standards which are expected to improve vehicle fuel efficiency.

Energy available for export increases.

EF 2013 concludes Canada will have more than enough energy to meet its growing needs, with significant amounts of energy available for export. Growth in export markets and the infrastructure to access them are key uncertainties in this report’s projections.

Chapter 1: Introduction

- Canada’s Energy Future 2013: Energy Supply and Demand Projections to 2035 (EF 2013) is a continuation of a series of long-term supply and demand projections that the National Energy Board (NEB) has been producing regularly since 1967.

- In developing EF 2013, the NEB met with various energy experts and interested stakeholders, including representatives from industry and industry associations, government, environmental non-governmental organizations and academia to gather input and feedback on the preliminary projections. The information obtained from these consultations helped shape the key assumptions and final projections.

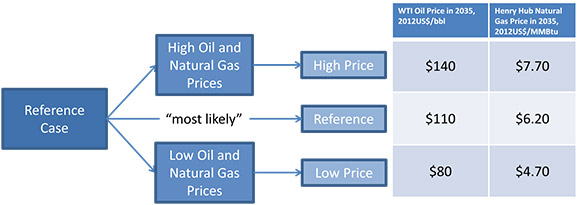

- EF 2013 projects energy supply and demand for Canada to the year 2035. It includes a Reference Case, with baseline projections based on the current macroeconomic outlook, a moderate view of energy prices, and government policies and programs that were law or near-law at the time the report was prepared. It is considered the “most likely” outcome for Canada’s energy future.

- In addition to the Reference Case, EF 2013 considers two sensitivity cases to provide broader perspective and to reflect the uncertainty around energy prices. The sensitivity cases are referred to as the High Price and Low Price Cases.

- The sensitivity cases differ from the Reference Case by changing the underlying price assumptions (Figure 1.1). The NEB’s suite of models helps to estimate the effects on the energy system and economy. Sensitivity analysis is a simple and effective means for analyzing uncertainty by isolating the effect of a change in one variable.

Figure 1.1 - Price Projections to 2035, All Cases

- There are four key assumptions underpinning this analysis:

- All energy production will find markets and infrastructure will be built as needed.

- Environmental and socio-economic considerations, beyond the included policies and programs, are outside the scope of this analysis.

- Only policies and programs that are law or near law at the time of writing are included in the projections. As a result, any policies under consideration, or new policies developed after the projections were completed, are not included in this analysis.

- Energy markets are constantly evolving. The analysis presented in EF 2013 is based on the best available information at the time of finalizing the analysis and results.

- Over the 23-year projection period, it is likely that developments beyond the realm of normal expectations will occur, such as geopolitical events or technological breakthroughs. Likewise, new information will become available and trends, policies and technology will evolve. Readers of this analysis should consider the projections a baseline for discussing Canada’s energy future, not a prediction of what will take place.

- The following chapters discuss the key factors influencing the Reference and sensitivity cases, highlighting key changes in Canadian energy supply and demand trends. Detailed data tables supporting this discussion are available in the Appendices on the NEB website.

Chapter 2: Energy Context

- The North American energy market has changed rapidly over the past several years. Likely the most notable change has been technological advances in drilling and well completion techniques that have rapidly transformed the outlook for North American natural gas and oil production. The impacts of these advances, and other shifting trends in the energy system, have important implications for Canadians and are described in the following section.

The Changing Energy Landscape

Shale and Tight Natural Gas Production

- Less than ten years ago the natural gas market was notably different than it is today. Natural gas producers were drilling as many gas wells as possible to try to maintain production levels and liquefied natural gas (LNG) imports from abroad were increasingly supplementing the North American gas supply. The 2005 edition of the United States (U.S.) Energy Information Administration’s (EIA) Annual Energy Outlook (AEO) projected LNG imports to increase to 494.4 106m³/d (17.5 Bcf/d) by 2025, 22 per cent of total U.S. consumption in that year.[3] The long-term expectation was for a supply-constrained natural gas market, with high gas prices and moderate gas demand growth.

- In a matter of a few years, the landscape for natural gas in North America changed dramatically, switching from a tight supply and demand balance to a market in which natural gas supplies are considerably more abundant at lower costs. A number of LNG export terminals are being proposed in Canada and the U.S., signs that the North American market is currently very well-supplied.

- This reversal can be largely attributed to technological advancements in natural gas drilling and well completion methods. In particular, a combination of extended reach horizontal drilling, multi-stage hydraulic fracturing and pad drilling have allowed producers to recover gas from areas that were previously thought to be technically impossible or not profitable. These technologies have largely been applied in deep shale and tight gas plays with little or no previous development.

- Extended reach horizontal drilling entails drilling down vertically, possibly to depths of two thousand metres or more, and then drilling horizontally within the target formation for considerable distances. As technology has progressed, the length of horizontal legs being drilled has increased.

- Hydraulic fracturing is a technique that has been around for many decades, but the process of creating several fractured zones in a single well within a short period of time - multi-stage hydraulic fracturing - is a much more recent advancement. To hydraulically fracture a well, companies typically pump a mixture of water, chemicals, and proppant[4] into the well at high pressures until the targeted formation cracks, creating a network of fractures through which gas can move from the formation and into the well. Multi-stage hydraulic fracturing processes continue to advance with the number of fracture stages within a well continuing to increase.

- Typically, hydraulic fracturing has focused on tight and shale formations, which both have very low permeability, meaning fluids have a difficult time moving through the formation. These formations can have large amounts of hydrocarbons stored in them.

- Pad drilling involves optimizing horizontal drilling and hydraulic fracturing processes by conducting these operations on multiple wells from a centralized location or well pad. Efficiencies are gained by avoiding the need to disassemble, move and then reassemble the drilling rig for each well, and the ability to stockpile materials and consolidate equipment. The efficiency gains help to control costs by allowing a single drilling rig to drill more wells annually despite their longer horizontal length and greater number of hydraulic fracture stages.

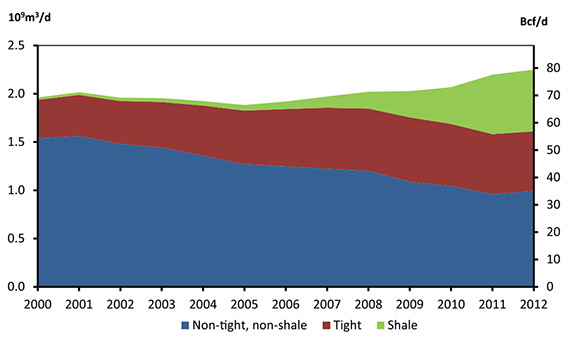

- The combination of these techniques has dramatically improved producers’ ability to recover natural gas. Gas production in the U.S. has increased sharply since 2006 when tight and shale production growth began outpacing declining production from conventional sources. In Canada, shale and tight gas production have partially offset declining conventional production, although total Canadian gas production has continually declined since 2006. Figure 2.1 demonstrates the combined U.S. and Canada natural gas production by type of production.

Figure 2.1 - Combined Canada and U.S. Marketable Natural Gas Production by Type

- As a result of rapidly increasing production, gas prices in North America have been around the US$3-4/MMBtu mark in recent years. This is much lower than prices in the 2006 to 2008 period, when the Henry Hub gas price averaged around US$7.50/MMBtu.

- In the Reference Case, natural gas prices increase gradually and shale and tight gas represent the vast majority of production growth in Canada. Production from the Montney tight gas area in Alberta and British Columbia (B.C.) and the Horn River shale gas area in Northeast B.C. help to reverse production declines and total Canadian production begins to increase by 2019. Later in the projection, several plays such as the Cordova Embayment in B.C. and Duvernay in Alberta begin to contribute to production growth as well

Tight Oil Production

- Soon after technological advances dramatically changed the gas production outlook, oil producers began applying similar technology to produce crude oil. Referred to as tight or shale oil[5], horizontal drilling and multi-stage hydraulic fracturing is applied to very low permeability shale, sandstone, and carbonate geologic formations, making oil production possible from many previously uneconomic or inaccessible reservoirs.

- Tight oil development began with the Bakken play in the Williston Basin area of North Dakota and Montana in the U.S. By year-end 2012, production in North Dakota reached nearly 123 10³m³/d (770 Mb/d)[6], a sevenfold increase over 2005 levels.

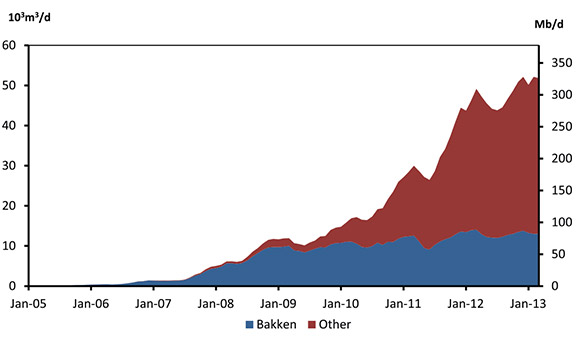

- Initial development of tight oil in Canada was also focused on the Bakken oil play, where the Williston Basin extends into Saskatchewan and Manitoba. Production at year-end 2012 is estimated at 14.2 10³m³/d (89.4 Mb/d), with the vast majority of growth occurring since mid-2007. In addition to the Bakken, several other tight oil plays are being developed in Manitoba, Saskatchewan and Alberta. Tight oil development in Canada is in its early stages and there appear to be numerous possible target formations. Figure 2.2 illustrates production levels for the Bakken and other tight oil plays, such as the Viking, Lower Shaunavon and Cardium formations. Estimated Canadian tight oil production in December 2012 was 52.1 10³m³/d (328 Mb/d), or about 10 per cent of total Canadian crude oil production.

Figure 2.2 - Canadian Tight Oil Production

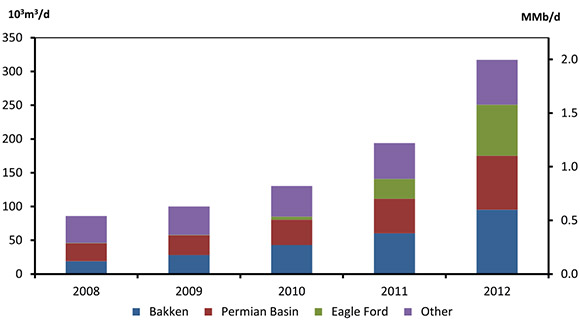

- As shown in Figure 2.3, U.S. tight oil production has been growing rapidly, led by the Bakken formations in North Dakota and Montana, the Permian Basin, and more recently the Eagle Ford Shale in Texas. The Monterey Shale in California, the Mississippi Lime play in Kansas and Oklahoma, and the Three Forks formation, which underlies the Bakken formation in North Dakota, show considerable potential.

Figure 2.3 - U.S. Tight Oil Production

- According to the EIA, the U.S. has reversed a long-term decline in oil production, with 2012 tight oil production growing to 317.3 10³m³/d (2.0 MMb/d), and total U.S. oil production reaching 1 031.8 10³m³/d (6.5 MMb/d).

- In 2012, the U.S. imported 1 349.5 10³m³/d (8.5 MMb/d) of crude oil. In its 2013 AEO, the EIA projects U.S. oil imports to shrink to 1 079.1 10³m³/d (6.8 MMb/d) by 2021, before resuming a growth trend. However, others project this trend of decreasing imports to continue in the longer term. The International Energy Agency (IEA) in its 2012 World Energy Outlook (WEO) projects a continued decline in U.S. oil imports to 2035, largely because of increasing domestic tight oil production. Given the early stage of tight oil development, future production and trade outcomes in the U.S. are particularly uncertain at this time. Currently, Canada’s crude oil is exported entirely to the U.S., so rising U.S. domestic supply could pose some risk to the growth of Canada’s traditional market for exports.

- Shale oil deposits exist in sedimentary basins throughout the world, and the assessment of these resources is gaining momentum. Deposits in countries such as Russia and China hold significant potential, but the economic and social viability of developing these resources is still largely unproven. Whereas producers in Canada and the U.S. benefit from a vast existing oil and gas industry infrastructure, the pace of shale oil development in many other parts of the world is likely to be considerably slower as the required infrastructure could take many years to put in place. The vast worldwide shale oil deposits could potentially provide enough additional supply to impact oil prices if these challenges could be overcome.

Transportation Energy Demand in North America

- In addition to changes in energy supply, energy demand trends in North America are gradually evolving, with implications for the North American energy landscape.

- This is particularly true for oil demand related to the transportation sector. The IEA’s 2012 WEO and the U.S. EIA’s 2013 AEO both expect U.S. oil demand growth in the transportation sector to slow from historical growth rates. This change, along with supply growth, is a key factor underpinning expectations that the U.S. will reduce its reliance on imported oil.

- The U.S. transportation sector represents a large share of North American and global petroleum demand. According to data from the EIA, the U.S. consumed 1 095.0 106m³ (6.89 billion barrels) of refined petroleum products in 2011, 21 per cent of global petroleum consumption and over 80 per cent of North American consumption. Seventy per cent of U.S. refined petroleum product demand was consumed in the transportation sector.

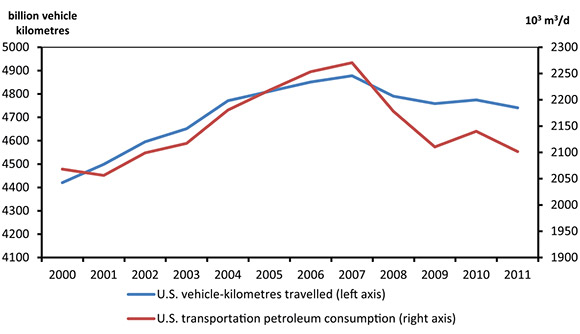

- The recent economic downturn affected transportation activity and energy use in the U.S. Figure 2.4[7] shows that both U.S. vehicle-kilometres travelled (VKT) and transportation petroleum demand began to decline in 2008, due to a combination of the economic downturn and record-high fuel prices.

Figure 2.4 - U.S. Vehicle Kilometres Travelled and Transportation Petroleum Consumption

- A key factor in the IEA and EIA projections of slowing transportation petroleum consumption is vehicle fuel efficiency improvements. Recent and forthcoming passenger and freight vehicle emission regulations are expected to result in improved vehicle efficiency in both Canada and the U.S.

- Demographics are an important factor in economic growth, and economic growth is an important driver of transportation demand. Demographics also have a direct impact on transportation demands, as different age groups tend to have different driving habits.[8] As the population ages, retirements are expected to put downward pressure on demands related to commuting. Recent research from The University of Michigan Transportation Research Institute also shows that a lower proportion of young people are becoming licensed drivers compared to previous generations.[9] This trend may also reduce transportation demands in the long term.

- The increasing use of alternative transportation fuels may also reduce the long-term demand for refined petroleum product transportation fuels in North America. Canada, the U.S., and Mexico have mandatory biofuel requirements, involving biofuels blended with gasoline and diesel. In the passenger vehicle market, there is interest in plug-in electric vehicles (EV) for personal transportation. Natural gas for transportation, particularly for freight using LNG, is also a key alternative that may experience growth, with much of the interest in long haul trucking and operations where the vehicles return to central locations often.

- In the Reference Case, Canadian transportation demand increases at an average annual rate of 0.8 per cent. This moderate growth is lower than the historical trend, and is heavily influenced by the inclusion of passenger and freight emission regulations that are expected to improve fuel efficiency. The projection also includes biofuel shares consistent with federal and provincial regulations, as well as moderate penetrations of EVs and natural gas vehicles (NGV).

The Electricity Supply Mix

- The electricity supply mix in North America has been changing in recent years, with implications for coal, natural gas and renewable energy consumption. While coal-fired generation has declined, the share of natural gas and non-hydro renewables has risen in response to changes in economic conditions, government regulations and environmental concerns.

- In 2011, coal accounted for just over 40 per cent of electricity generation in the U.S. and 13 per cent of electricity generation in Canada. Coal remains the most common source of electric power in the U.S., but the share of coal-fired generation has been declining in both countries, largely because of the increased use of natural gas and policy initiatives such as the Ontario coal phase-out.

- In the short term, displacement of coal-fired generation with natural gas-fired generation occurs when natural gas is priced competitively compared with coal. Recently, natural gas-fired generation matched or exceeded coal-fired generation. In April 2012, coal and natural gas each accounted for 32 per cent of total generation in the U.S. In the same year, the share of natural gas-fired generation rose above the share of coal-fired generation in Canada.

- There has been less coal-to-gas switching in 2013 as natural gas prices have risen from the lows seen in 2012. However, U.S. and Canadian government policies will likely discourage the use of coal in the long run.

- In Canada, federal regulations enacted in 2012 stipulate that coal-fired plants starting operations after 1 July 2015 must not emit more than 420 metric tons of carbon dioxide (CO2) per gigawatt-hour, often referred to as a level consistent with high-efficiency natural gas plants. Existing facilities that do not meet this standard retire either after 50 years of operations, or at the end of 2019 or 2029 (depending on their commissioning date), whichever date comes first. In order to comply with these new rules, coal plants will likely have to install carbon capture and storage (CCS) equipment. As a result, the share of coal-fired generation is expected to steadily decline in Canada.

- In the U.S., several regulations now place a limit on the level of mercury, sulfur dioxide, nitrous oxides and other pollutants emitted by coal-fired plants. The U.S. regulations include, among others, the National Ambient Air Quality Standard, the Mercury and Air Toxics Standards, the Clean Air Mercury Rules and the Clean Air Interstate Rules. In addition, lower capital costs provide an incentive for building natural gas plants instead of coal plants.

- Investments necessary to ensure coal plant operators’ compliance with those standards increase the cost of coal-fired generation. Rules that are even more stringent are proposed in the U.S., which, if adopted, could prevent the construction of new coal-fired plants using existing technology because such plants would be unable to comply with the standards and remain competitive in the market. In its most recent outlook, the EIA projects that only three per cent of capacity additions in the U.S. from 2012 to 2040 will come from coal plants. In contrast, the EIA projects natural gas-fired plants will account for 63 per cent and renewables for 31 per cent of capacity additions.

- On a percentage basis, non-hydro renewables such as wind, solar and biomass have been the fastest growing source of generation in both countries. Government incentives, such as federal tax credits and state-level policies in the U.S. and renewable energy targets and standards in Canada, contributed to this growth. Between 2005 and 2012, wind and solar generation increased sevenfold in the U.S. and generation from all non-hydro renewables almost doubled in Canada. Consequently, the share of generation produced from non-hydro renewable sources in 2012 reached three per cent in Canada and five per cent in the U.S.

- The IEA noted in its 2012 WEO that the role of nuclear power has been scaled back since the accident at the Fukushima Daiichi power station in 2011. Total world nuclear generation decreased by nine per cent and seven per cent in 2011 and 2012, respectively. Many countries have reviewed their nuclear energy policies, while increased natural gas use in North America have challenged nuclear power’s competitiveness for new capacity.

- Policies and regulations that affect the power sector, as well as the relative economics of various power sources, continue to evolve. These factors are important determinants of the projected electricity supply mix. In this analysis, both coal-to-gas switching and growth in non-hydro renewable generation are expected to continue over the long term. Although no new nuclear capacity is projected to come online, planned refurbishments in Ontario are included in the projections.

Canadian Energy in the North American and Global Marketplace

Oil Transportation Infrastructure and Price Differentials

- Energy transportation infrastructure in North America typically responds to changes in supply and demand trends, with sufficient capacity usually in place to accommodate production increases. Production of tight oil in the U.S. has grown rapidly and at a much quicker pace than many market observers had expected. In addition, many expected the Keystone XL project to start providing new oil pipeline capacity beginning in 2012, but that project still awaits a final U.S. decision. As a result, oil transportation infrastructure developments fell behind changing supply trends throughout much of 2011 and 2012.

- Rapidly increasing tight oil supply, combined with steadily increasing oil sands production, led to a glut of oil in the mid-continent region of the U.S., creating pipeline bottlenecks at key points in the North American pipeline system.

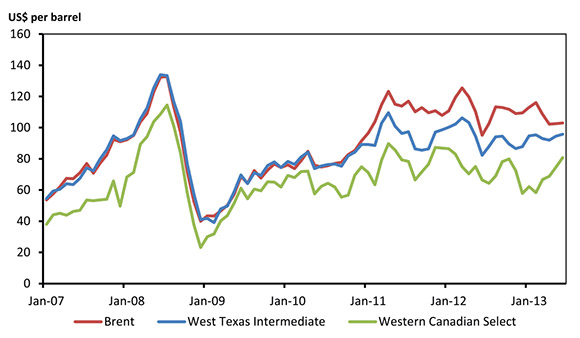

- The West Texas Intermediate (WTI) oil price, considered the North American benchmark oil price, is determined at Cushing, Oklahoma where many oil pipelines interconnect. As production rose, the hub became a key pipeline bottleneck in 2011, lacking adequate capacity to move growing crude inventories outward from the mid-continent.

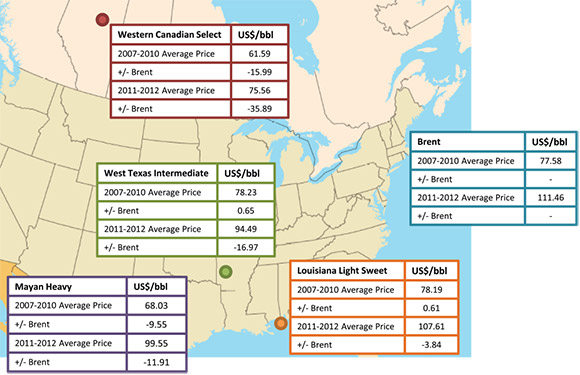

- Prior to 2011, WTI closely tracked international oil prices such as Brent, the European benchmark oil price. In response to the oversupply of crude at Cushing, WTI became discounted relative to Brent commencing in 2011, as shown in Figure 2.5. At the same time, geopolitical events and production issues in the North Sea (the pricing point of Brent crude) put upward pressure on the Brent price. Combined, these factors resulted in WTI averaging nearly US$17/bbl below Brent through 2011 and 2012.

Figure 2.5 - Benchmark Oil Prices

- Other oil transportation bottlenecks developed further upstream of Cushing, resulting in further price discounts for some producers, especially heavy oil producers in Canada. The key pricing benchmark for Canadian heavy crude, Western Canadian Select (WCS), traded US$16.64/bbl below WTI from 2007 to 2010. In traditional market conditions, this lower price reflects the transportation costs of shipping Canadian heavy oil to market and the lower quality of WCS compared to WTI crude. Throughout 2011 and 2012, the WCS price traded on average nearly US$19/bbl below the WTI price and the differential was at times volatile, with the monthly average differential widening to more than US$30/bbl on a few occasions.

- Refinery outages and reconfigurations also affected differentials, and explained a large part of the volatility in the WTI-WCS spread. Maintenance at several heavy oil refineries in the mid-continent contributed to the glut of oil and exacerbated price differentials. As well, the BP Whiting Refinery, located in Indiana, was operating at reduced capacity while undergoing changes to allow refining of substantially higher heavy crude volumes. This resulted in producers selling additional heavy crude into an already oversupplied mid-continent market.

- Figure 2.6 demonstrates that, while prices for inland crude have been discounted relative to international prices for the past several years, prices for crude in locations that are linked to the international marketplace via access to coastal ports, such as Louisiana Light Sweet in the U.S. Gulf Coast, tracked international oil prices more closely. The Mayan crude price, a benchmark price for heavy oil produced in Mexico, is also included in the figure. Mayan Heavy represents crude with quality similar to WCS, but with greater access to international oil markets.

Figure 2.6 - Benchmark Oil Prices and Price Differentials

- In early 2013, the Brent-WTI and WTI-WCS differentials began to narrow. Several pipeline projects aimed at relieving key bottlenecks were put into service, such as the Seaway pipeline reversal that added capacity to move more oil from Cushing to the U.S. Gulf Coast. Oil producers also increasingly utilized rail to avoid pipeline bottlenecks and to access higher priced markets in North America. An expansion of the Marathon refinery in Detroit was completed and the major components of the BP Whiting Refinery conversion were put into service in July of 2013, adding additional heavy oil refining capacity in the U.S. Midwest. By mid-2013, price differentials between Brent, WTI and WCS moved closer to historical levels, suggesting the oversupply condition in the mid-continent region was alleviated, at least for the time being.

- Many market observers have noted that expectations for continued growth in oil sands and tight oil production are dependent on adequate transportation infrastructure being in place and sufficient markets for crude oil being found. For the purposes of this analysis, adequate infrastructure and sufficient markets are assumed to exist throughout the projection period. If these assumptions do not hold, pipeline constraints and price differentials will likely impact oil producers, and the broader energy system, in coming years. This is a key uncertainty to projections in EF 2013.

Oil Transportation by Rail

- The pipeline bottlenecks and price differentials described above have encouraged oil shippers to seek alternative methods to move oil to markets.

- Shippers in the U.S. and Canada are increasingly transporting oil by railroad. The flexibility provided by rail transportation allows oil to be delivered from regions lacking pipeline capacity to nearly anywhere in North America with a rail unloading facility.

- Oil transportation by rail has been used at particularly high levels in the rapidly growing shale and tight oil plays of the U.S. By using existing rail facilities and adding new loading facilities, rail transportation can usually be added in a shorter timeframe than building pipelines. Oil production in North Dakota’s Bakken oil play increased from an average of 27.2 106m³/d (171 Mb/d) in 2008 to average 105.5 106m³/d (664 Mb/d) in 2012.[10] Over that period, pipeline capacity grew from 43.2 106m³/d (272 Mb/d) to 73.6 106m³/d (463 Mb/d) while rail loading capacity grew from 4.8 106m³/d (30 Mb/d) to 104.9 106m³/d (660 Mb/d).[11]

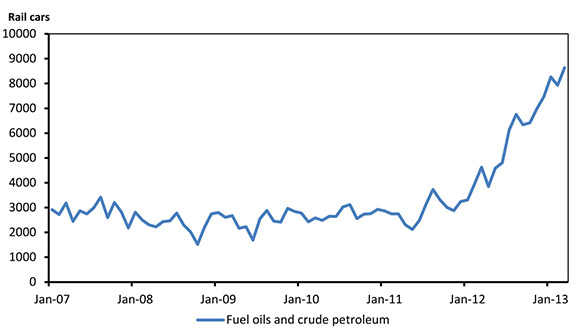

- In Canada, rail represents a small but growing proportion of oil transportation. In 2012, rail cars shipping fuel oil and crude petroleum grew from approximately 3 000 cars to 8 000 by the end of the year according to Statistics Canada (Figure 2.7).

Figure 2.7 - Railway Car Loading, Fuel Oils and Crude Petroleum, Western Canada

- In this analysis, energy transportation infrastructure is assumed to be built as needed. Specific assessments regarding oil transportation by rail is not part of this analysis. However, in the short term, it is likely that rail will continue to play an important role in providing additional oil transportation capacity.

- In the medium term, the utilization of oil by rail transportation in Canada is related to the addition of pipeline capacity out of the Western Canada Sedimentary Basin (WCSB). If additional pipeline capacity is not built, it is possible that the price differentials noted earlier will widen again, encouraging producers to increase their use of rail transportation. On the other hand, additional pipeline capacity could help to lessen price differentials and slow the demand for shipping crude by rail.

- Any further rules or regulations related to concerns about increased railway traffic from a safety and environmental perspective could impact the utilization of crude transportation by rail.

Changing Natural Gas Flows in North America

- In recent years, dramatic changes in gas production trends, both in terms of volume and location, have impacted traditional North American gas flows.

- In 2005, nearly a quarter of gas production in Canada, the U.S. and Mexico originated in the WCSB. Traditional markets for WCSB production include Ontario, Quebec and the U.S. Northeast, as well as the U.S. Midwest and Pacific Coast.

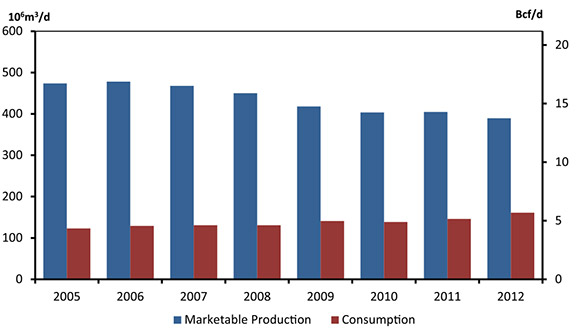

- Declines in natural gas prices have reduced drilling activity for conventional gas in the WCSB in recent years, with production trending down since 2006. Production in Alberta, B.C. and Saskatchewan totaled 478.0 106m³/d (16.9 Bcf/d) in 2006. By 2012, production had declined to 389.4 106m³/d (13.7 Bcf/d) (Figure 2.8), less than 17 per cent of North American gas production.

Figure 2.8 - B.C., Alberta and Saskatchewan Combined Production and Consumption

- At the same time, demand for gas in the region has increased. Natural gas consumption in B.C., Alberta and Saskatchewan increased from 129.1 106m³/d (4.6 Bcf/d) in 2006 to approximately 160.9 106m³/d (5.7 Bcf/d) in 2012. Much of the increase was because of growing natural gas consumption in the oil sands. Growing consumption and decreased gas production and has resulted in declining volumes of gas being shipped out of the WCSB.

- Other dynamics have also factored into changing gas flows in North America. In particular, some emerging shale gas areas in the U.S. are located close to markets traditionally served in part by WCSB gas. A prime example is the Marcellus shale in the U.S. Northeast, spanning much of Pennsylvania, West Virginia and New York State. Pennsylvania production increased from 20.8 106m³/d (733 MMcf/d) in early 2010 to 134.8 106m³/d (4.8 Bcf/d) by the end of 2011.

- Increasing production in the Marcellus has reduced the need for Canadian exports to the U.S. Northeast. Combined export volumes at Ontario and Quebec border points fell from 65.2 106m³/d (2.3 Bcf/d) in 2006 to 25.6 106m³/d (904.4 MMcf/d) in 2012.

- Meanwhile, gas imports into Canada, most of which are delivered into Ontario and Quebec, increased from 26.6 106m³/d (938.1 MMcf/d) in 2006 to 80.6 106m³/d (2.8 Bcf/d) in 2012. A number of traditional export pipelines in Ontario have been altered to permit bi-directional gas flow and allow additional imports from the U.S. when required.

- In the Reference Case, WCSB gas production continues to decline until 2018. Also, gas consumption in Alberta, B.C. and Saskatchewan continues to increase. Combined, these projections imply that gas shipped out of the WCSB will continue to decline in the medium term. The specific path of future gas flows is not covered in this analysis and is subject to a number of uncertainties, including gas supply and demand, infrastructure developments and pipeline tolls.

- While future gas flows are beyond the scope of this report, the North American gas market is highly integrated, gas resources in both Canada and the U.S. are abundant, and market forces operate to balance supply and demand. As a result, it is expected that sufficient supplies will exist to meet Canadian gas demand.

LNG Exports from Canada and the U.S.

- The North American gas market is continental in nature, with the balance between domestic supply and demand largely determining natural gas prices.

- Outside of North America there are a variety of markets with their own supply, demand and pricing dynamics. Some regions have limited domestic gas supplies and rely on imported gas to meet much of their natural gas demand. Others produce natural gas in excess of their domestic needs. When pipelines are not feasible, LNG can connect these markets, linking exporters and importers.

- LNG is natural gas that is chilled to -162°C, at which point it becomes a liquid. In its liquid form, it is much more energy-dense than when in a gaseous state, making it economic to ship in specially designed vessels and vehicles.

- LNG has been traded globally since the mid-1960s. Since then, the volume of global LNG trade has increased steadily to an estimated 237.7 million tonnes per annum (MMtpa) in 2012.[12] In gaseous form, this is approximately equivalent to 898.4 106m³/d (31.7 Bcf/d), just over 10 per cent of global gas consumption.

- The top five LNG exporters in 2012 were Qatar, Malaysia, Australia, Nigeria and Indonesia, which together were responsible for 67 per cent of LNG exports. Seventy per cent of total LNG shipments were delivered to Asia in 2012, with Europe the second largest importer.

- Most LNG importers acquire the majority of their gas supply through long-term contracts to ensure supply reliability. The contract prices are often linked to the crude oil price. In 2012, prices for LNG in Korea and Japan ranged from US$13/MMBtu to US$18/MMBtu.

- International natural gas prices that are above prices in North America have led natural gas producers and other market participants to propose LNG export terminals in North America.

- In Canada, a number of proposals have been announced to export LNG. At the time of writing, the NEB has issued long-term licences for three of these proposals, all for exports on the B.C. Coast. Five more applications were under review by the Board at the time of writing, four proposing to export LNG from the B.C. Coast. The Jordan Cove application is to export natural gas by pipeline to the U.S., to support a proposed LNG export facility in Oregon. Currently none of the proponents have announced final decisions on whether they will go ahead with their projects.

- In the U.S. there have also been several proposals to export LNG to countries that the U.S. does not have a free trade agreement with. Most of these proposed facilities are located on the U.S. Gulf Coast. At the time of writing, the U.S. Department of Energy had granted three export authorizations, allowing the holders to export LNG globally. The natural gas equivalent of the authorizations totals 158.6 106m³/d (5.6 Bcf/d).

- The analysis in EF 2013 assumes 28.3 106m³/d (1.0 Bcf/d) of LNG exports from the B.C. Coast in 2019, increasing to 56.6 106m³/d (2.0 Bcf/d) in 2021 and 85.0 106m³/d (3.0 Bcf/d) by 2023. It is important to note that this is an assumption as opposed to a view on eventual LNG export volumes. This assumption allows for analysis of other key outcomes, such as gas production, energy demand and macroeconomic projections. This volume is not associated with any particular Canadian project shown in Table 2.1 or any other proposed projects.

Table 2.1 - Long-term Natural Gas Export Licences and Applications Under Review as of 1 October 2013

| Proponent | NEB Export Licence | Date issued | LNG Volume (approximate natural gas equivalent) |

|---|---|---|---|

| KM LNG | GL-298 | November 2011 | 10 MMtpa (36.3 106m³/d, 1.28 Bcf/d) |

| B.C. LNG Export Co-operative | GL-299 | April 2012 | 1.8 MMtpa (6.6 106m³/d, 232 MMcf/d) |

| LNG Canada | GL-300 | February 2013 | 24 MMtpa (91.6 106m³/d, 3.23 Bcf/d) |

| Prince Rupert LNG | N/A | Under Review | 21.6 MMtpa (82.4 106m³/d, 2.91 Bcf/d) |

| WCC LNG | N/A | Under Review | 30 MMtpa (113.3 106m³/d, 4.00 Bcf/d) |

| Pacific NorthWest LNG | N/A | Under Review | 19.7 MMtpa (77.6 106m³/d, 2.74 Bcf/d) |

| Woodfibre LNG | N/A | Under Review | 2.1 MMtpa (8.1 106m³/d, 288 MMcf/d) |

| Jordan Cove LNG | N/A | Under Review | 43.9 106m³/d, 1.55 Bcf/d |

- The eventual volume of LNG exports may be higher or lower than assumed in this analysis. Key uncertainties include North American natural gas prices, competition from other LNG supply basins, the pace of LNG demand growth, and the ability of Canadian LNG proponents to secure contracts with buyers. These, and other market factors, will determine the eventual volumes of LNG exports from Canada.

Electricity Exports, Imports and Interprovincial Trade

- Electricity markets differ from other commodity markets in several key ways. The inability of electricity to be easily stored in commercial quantities is the most significant difference. In contrast with oil and gas markets, where pricing is often set on a global or continental basis, electricity trade and pricing is more regional. Despite these differences, the highly-integrated North American electricity market has been affected by many of the key trends discussed previously in this chapter.

- Canada is a net exporter of electricity to the U.S., and large amounts of electricity are also transferred between provinces. Interprovincial and international electricity trade benefits the reliability of electric grids. By linking regions, provinces and states can take advantage of having different peak periods, based not only on the time of day, but also on the time of year. Seasonal peaks in Canada occur primarily during the winter heating season while peaks in the U.S. occur mostly in the summer air conditioning season.

- While factors such as proximity to demand and existing infrastructure are important, regional development of electricity supply is primarily influenced by the cheapest fuel source available in a given region. Historically, provinces that have exported large amounts of power are those with hydro-based generation. More electricity tends to be exported in high precipitation years, when hydroelectric reservoirs are well supplied.

- The economic downturn of 2009 reduced continental electricity demand. Canada is only now returning to pre-recession electricity demand levels. In the U.S., overall demand has remained below its peak level in 2007. Lower demand levels and lower natural gas prices have resulted in lower wholesale electricity prices throughout North America. Prices in many regions to which Canada exports fell by roughly half between 2008 and 2012.

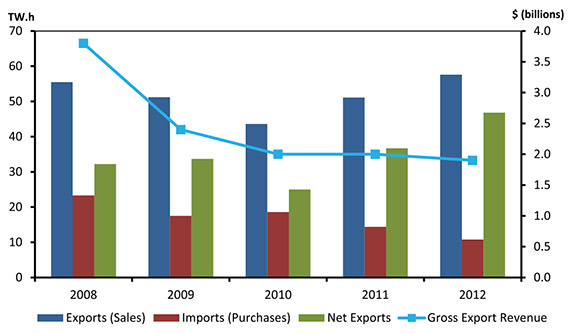

- Supply-demand conditions, including high Canadian hydroelectric reservoir levels, resulted in record Canadian net exports in 2012. Annual net exports were 45 per cent higher in 2011 compared with 2010. In 2012 net exports were 47 TW.h, because of record high exports of 58 TW.h and lower imports of 11 TW.h.

- Although the quantity of electricity exports is higher, prices are lower, reducing export revenues compared with historical revenues. For example, in 2008 exports of 56 TW.h were valued at $3.8 billion in revenue, whereas the 2012 exports of nearly 58 TW.h sold for only $1.9 billion.

Figure 2.9 - Annual Canadian Electricity Exports, Imports and Export Revenue

- Based on the economic and electricity demand outlooks, wholesale electricity prices are expected to remain low for the next several years. At present, there are many uncertainties surrounding the economics of building generation and transmission facilities to produce and export electricity. Without a guarantee of long-term export contracts and higher wholesale electricity prices, some large hydro plant proposals, such as Conawapa in Manitoba and Gull Island in Labrador, are not assumed to be built in the projection period. Some large capital-intensive infrastructure projects, such as new nuclear builds in Ontario, are also not included in the projections, in part due to the availability of lower cost generation, including imports from other regions.

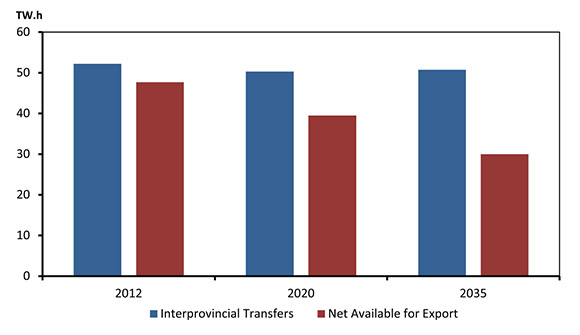

- In the Reference Case, net electricity available for export is projected to remain near current levels until 2030. By 2035, net electricity available for export is projected to return to historic levels, declining to 30 TW.h annually compared with 47 TW.h in 2012. Interprovincial electricity transfers are projected to slightly decline from 52 TW.h in 2012 to 51 TW.h in 2035.

Chapter 3: Key Drivers

- EF 2013 considers three cases - a Reference Case, which reflects a moderate view of future energy prices and economic growth - and two sensitivity cases. These sensitivity cases represent a range of possible outcomes for the Canadian energy system over the projection period. Higher and lower crude oil and natural gas prices characterize the sensitivity cases, referred to as the High Price and Low Price Cases.

Energy Prices

Crude Oil Prices

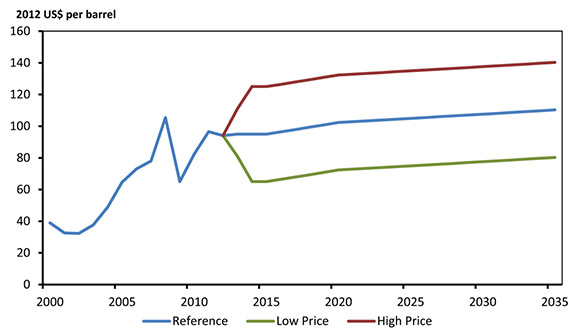

- In the Reference Case, the WTI crude oil price is assumed to average US$95/bbl in 2013. As shown in Figure 3.1, the price in 2012 dollars stays flat at US$95/bbl until 2016 when it begins to slowly increase over the projection period, reaching US$110/bbl by 2035. Growing tight and shale oil production have increased global supply. However, strong oil demand from developing countries offsets this supply growth and contributes to the gradual price increase over the projection period. The WTI crude oil price is 16 per cent higher in 2035 compared with 2013.

Figure 3.1 - WTI Crude Oil Price at Cushing, Oklahoma, All Cases

- In the Low Price Case, the WTI crude oil price is assumed to be US$30/bbl below the Reference Case price throughout the projection period, reaching US$80/bbl in 2035. In the High Price Case, it is assumed to be $30 higher than the Reference Case price, rising to US$140/bbl by 2035.

- As noted in Chapter 2, throughout 2011 and 2012, the WTI oil price was at a significant discount to the Brent price, a major crude oil price marker in Europe. Historically, the two prices have closely tracked one another. By mid-2013, WTI and Brent prices were moving closer together again, as oil infrastructure developments helped alleviate the oversupply of oil in the midcontinent of North America. The traditional relationship between WTI and international oil prices is assumed to continue to hold throughout the projection period.

Natural Gas Prices

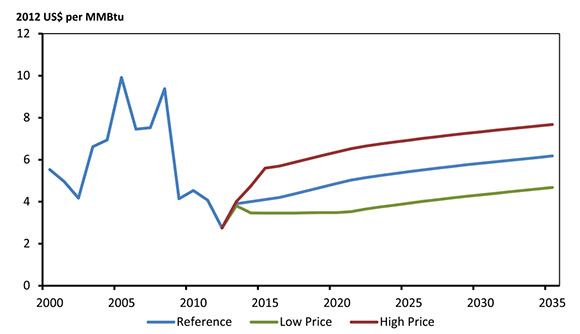

- The Henry Hub price for natural gas in the Reference Case is assumed to increase from US$3.90/MMBtu in 2013 to US$6.20/MMBtu in 2035 (in 2012 dollars) as shown in Figure 3.2. The Henry hub natural gas price is nearly 60 per cent higher in 2035 compared with 2013.

Figure 3.2 - Henry Hub Natural Gas Price at Louisiana, All Cases

- In the Low Price Case, the natural gas price is assumed to reach US$4.70/MMBtu by 2035 and US$7.70/MMBtu in the High Price Case.

Electricity Prices

- Electricity prices are largely determined in regional markets. Consumer prices for electricity are mainly composed of generation, transmission and distribution costs. Prices are generally lowest in the hydro-based provinces (B.C., Manitoba, and Quebec), which benefit from a high proportion of low-cost heritage assets. These assets are often many decades old and their capital costs are largely paid off.

- Prices in most jurisdictions are based on the actual cost of providing service to consumers, including a regulated rate of return on the generation, transmission and distribution assets. Provincial and, in some cases, municipal regulators are responsible for approving these costs. All provinces and the territories follow this model, except Alberta and Ontario, which operate wholesale electricity markets. In Alberta, competitive wholesale markets determine wholesale electricity prices, from which consumer rates are derived. In Ontario, while the wholesale market determines spot prices, most of the generators receive fixed or regulated prices, making the market a hybrid of the two methodologies.

- Typically, prices tend to be higher for residential customers and lower for large volume industrial customers, reflecting the cost of serving these markets. In addition, large customers may have direct access to wholesale markets where power costs can be lower than the rates offered by the retail distribution utilities.

- In the Reference Case, the average retail electricity price (including the residential, commercial and industrial prices) is approximately 20 per cent higher in 2035 compared with 2013, in real dollars. This reflects the increasing cost of sourcing new generation and planned improvements to transmission systems. Electricity prices in the sensitivity cases vary moderately from the Reference Case, influenced by the change in natural gas and oil prices, as well as differences in electric demand and generation.

Economic Growth

- The Canadian economy is a key driver of the energy system. Economic growth, industrial output, inflation, exchange rates and population growth are key macroeconomic factors that influence the energy supply and demand outlook.

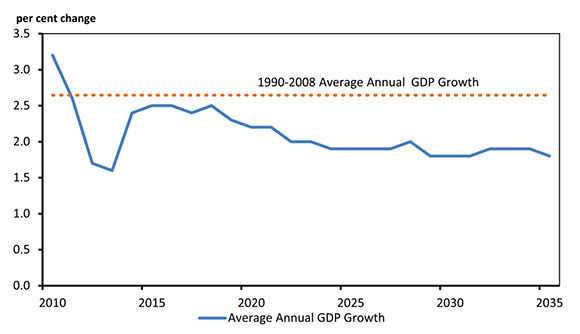

- As shown in Figure 3.3, Canadian real gross domestic product (GDP) growth is projected to be 1.5 per cent in 2013. From 2012 to 2035, the average annual real GDP growth rate is 2.0 per cent. This is a moderation in growth compared to the historical trend; annual real GDP growth was 2.6 per cent over the 1990 to 2008 period.

Figure 3.3 - Annual GDP Growth, Reference Case

- Demographics play a key role in the long-term macroeconomic projections. Canadians born between 1946 and 1965, referred to as baby boomers, represent a large segment of the current workforce. The oldest boomers have begun to reach retirement age and the rate of retirements accelerates over the projection period. Therefore, the proportion of the population that is of working age will shrink over the projection, creating slower labour force growth compared to the historical trend. This is a key factor moderating economic growth.

- Developing nations, such as China and India, recovered quickly from the global economic downturn in 2009 and have grown rapidly compared to developed nations in recent years. These markets are a growing source of demand for Canadian natural resources and manufactured goods. Economic growth in these regions remains elevated over the projection period and drives growth in Canada’s export-oriented sectors.

- Regionally, economic growth in the Reference Case is strongest in the western provinces and territories, driven by growth in the mining and oil and gas industries. With an average annual growth rate of 2.5 per cent per year over the projection period, Alberta has the strongest economic growth. Combined, Quebec and Ontario’s annual GDP growth averages 1.9 per cent, slightly lower than the national average. Growth is slowest in Atlantic Canada because of slower population growth and declining offshore oil and natural gas production in the long term.

Key Uncertainties to the Outlook

- Energy prices are a key uncertainty to the macroeconomic projections. The High and Low Price Cases capture some of the potential uncertainty. However, the possibility of prices outside the chosen range exists, as do dramatic short-term price swings, which could have future implications for the projections.

- Economic conditions can have a significant impact on the Canadian energy system. Several key uncertainties could impact the economic drivers and hence the energy supply and demand projections described in the following chapters.

- International demand for Canadian goods will influence export-oriented industries, many of which are relatively energy-intensive. Faster or slower economic growth in the U.S., Canada’s largest trading partner, would impact the economic and energy demand projections. Also, the sustainability of rapid economic growth in many emerging markets is a key uncertainty to the projections.

- Existing and future monetary policy could impact the macroeconomic and energy projections. Internationally, monetary stimulus was put in place following the 2008-2009 global recession. The timing and impact of the removal of that stimulus is uncertain, as is the long-term impact on interest rates and inflation.

- Large natural resource extraction developments in the mining and oil and gas sectors contribute to the macroeconomic projections in a number of provinces. The pace of these developments is uncertain and could contribute to higher or lower economic growth.

- As noted earlier, the Reference and sensitivity cases include only policies and programs that are law or near law at the time of writing. As a result, any policies under consideration, or new policies developed after the projections were completed, are not included in this analysis.

Chapter 4: Energy Demand Outlook

- In this analysis, end-use (or secondary) energy demand includes energy used in four sectors: residential, commercial (includes institutional and pipelines), industrial, and transportation.[13] End-use energy demand excludes the energy used to generate electricity.

- Energy used to generate electricity is included under primary demand. The majority of this chapter focuses on end-use consumption by sector, with a brief section on primary demand included at the end. Chapter 7 includes further details on electricity generation and fuel mix.

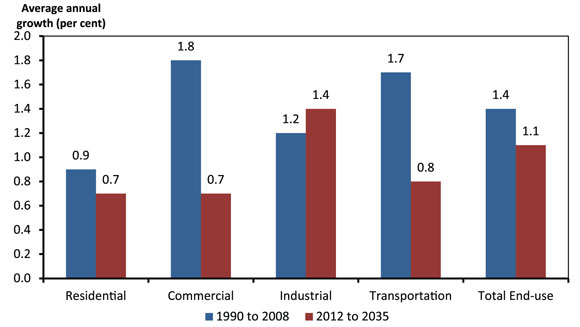

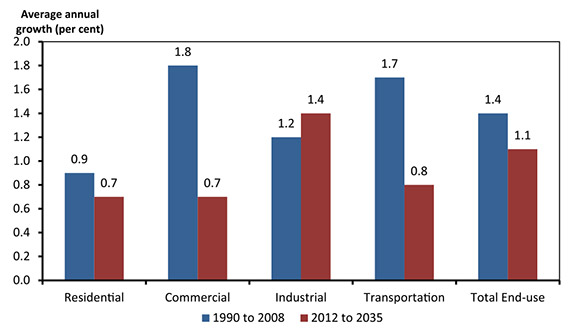

- In the Reference Case, total end-use energy demand increases by an average of 1.1 per cent per year (Figure 4.1). This growth is led by the industrial sector, which grows at an annual average rate of 1.4 per cent. The average annual growth rates of the remaining sectors are less than one per cent. The residential and commercial sectors both grow at an annual average rate of 0.7 per cent, while the transportation sector grows at 0.8 per cent, over the projection period.

Figure 4.1 - End-Use Energy Demand by Sector, Reference Case

- Overall, energy demand growth slows compared to the historical trend, where demand grew at an average of 1.4 per cent from 1990 to 2008. The industrial sector, which grows slightly faster than the 1990 to 2008 rate of 1.2 per cent per year, is the largest growth area in the projection. Industrial growth is related to strong growth in natural resource industries, such as mining and the oil and gas sector, as well as other energy-intensive manufacturing sectors that gradually recover from the recent economic downturn. Demand growth projections in the residential, commercial, and transportation sectors are lower than historical levels. From 1990 to 2008, the residential sector grew at an average annual rate of 0.9 per cent, commercial by 1.8 per cent, and transportation by 1.7 per cent.

- Total energy intensity, measured as energy use per dollar of real GDP, decreases by an average annual rate of 1.0 per cent over the projection period. This continues the historical trend, where energy intensity declined by an average of 1.2 per cent per year from 1990 to 2008. Energy intensity is influenced by a variety of factors, including improvements in energy efficiency.

- The analysis includes those policies, programs and regulations that are law or near law. Several new initiatives are included in these projections that were not included in previous NEB outlooks. Two examples are freight transportation emission standards and the long-term passenger vehicle standards (covering 2017 to 2025). Although these regulations are set in terms of emission reductions, they are expected to result in improved vehicle fuel efficiency and lower energy demand projections in these sectors.

- Energy demand grows slightly faster in the Low Price Case, with an average annual rate of 1.2 per cent over the projection period. The High Price Case demand projection is lower than the Reference Case, averaging 0.8 per cent per year. Generally, higher prices put downward pressure on energy demand growth, and this is evident in the projections. However, this effect is somewhat offset by the oil and gas sector, where demand growth is lower in the Low Price Case and higher in the High Price Case, as energy use follows the production projections discussed in Chapters 5 and 6.

Energy Consumption by Sector

Residential Sector

- Residential energy use is the energy consumed by Canadian households. This includes energy used for space and water heating, air conditioning, lighting, large appliances, and other energy-using devices like televisions and computers.

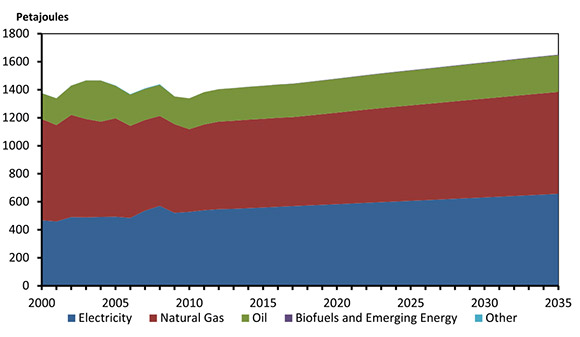

- In 2011, Canadian residential energy demand was 1 451 PJ, and accounted for 14 per cent of total Canadian energy demand. Residential energy demand increases at an average annual rate of 0.7 per cent over the projection period, reaching 1 730 PJ in 2035 (Figure 4.2).

Figure 4.2 - Residential Energy Demand, Reference Case

- Energy-use per square metre of residential floorspace declines at an annual average rate of 0.6 per cent over the projection period. Improvements in building shell construction practices, increased penetration of high efficiency heating appliances, substantial energy efficiency improvements in major home appliances and electronics, and new standards for lighting and water heating are key factors in this trend.

- Demand management programs, policies and regulations are important to residential demand projections. All provinces and territories have voluntary programs encouraging greater energy efficiency in new homes and equipment. Many of these programs offer incentives to consumers such as rebates, low-interest loans, and education and awareness campaigns. Three new amendments to the federal Energy Efficiency Act have increased minimum energy performance standards for several common home appliances. The phase-out of inefficient lighting comes into effect in 2014. A national effort resulting in a new National Building Code for commercial buildings had a spill-over effect on the home market as well.

- The types of energy used in the residential sector vary widely across Canada. Energy prices, end-use energy requirements and fuel regional availability determine the differences in energy mix between the various regions. Atlantic Canada primarily meets its energy needs with electricity, oil and biomass, as natural gas is newer to the region. Quebec, Manitoba and B.C. rely more on electric energy, given their relatively low cost hydroelectric supply. Alberta and Saskatchewan rely more heavily on natural gas than other provinces. The Ontario mix is composed mainly of natural gas and electricity, along with a moderate share of biomass and oil.

Commercial Sector

- The commercial sector is a broad category that includes offices, retail, warehousing, government and institutional buildings, utilities, communications, and other service industries. It also includes energy consumed by street lighting and pipelines. The buildings portion of the commercial sector uses energy for space and water heating, air conditioning, lighting, appliances and other devices. The pipeline portion uses energy to power pumps or compressors that move the oil and natural gas through the pipeline.

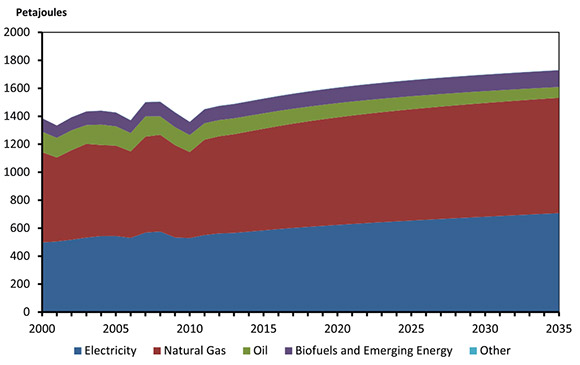

- In 2011, Canadian commercial energy demand was 1 382 PJ, and accounted for 13 per cent of total Canadian energy demand. Commercial energy demand increases at an average of 0.7 per cent per year over the outlook period, reaching 1 650 PJ in 2035 in the Reference Case (Figure 4.3).

Figure 4.3 - Commercial Energy Demand, Reference Case

- An extensively revised National Energy Code for Buildings (NECB) was finalized in 2011. This companion to the National Building Code puts a greater emphasis on energy performance in buildings than in the past. Minimum performance standards apply to building shell, HVAC, lighting, and electrical loads. It applies to new buildings, as well as to substantial renovations in existing ones. The code change is expected to improve energy performance in new commercial, institutional, and multi-unit residential complexes by 25 per cent compared to the previous code (1997). Adoption of the new NECB is ultimately up to the provincial, territorial, or, in some cases, municipal authority. This consensus-based revision had broad stakeholder support and is expected to have widespread uptake. As with the residential sector, some provinces had already stipulated building standards that meet or exceed NECB, and the trend going forward is a decreasing degree of difference between regions in terms of building efficiency.

Industrial Sector

- The industrial sector includes manufacturing, forestry, fisheries, agriculture, construction, and mining. In 2011, 80 per cent of industrial energy was consumed by a handful of energy-intensive industries, such as iron and steel, aluminum, cement, chemicals and fertilizers, pulp and paper, petroleum refining, mining, and oil and gas extraction.

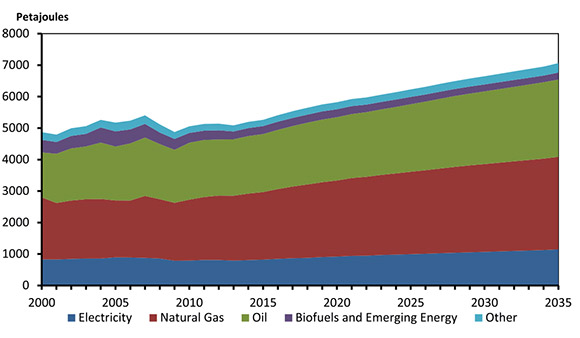

- The industrial sector makes up the largest share of Canadian end-use energy demand, accounting for 48 per cent, or 5 132 PJ, in 2011. It is also the fastest growing sector over the projection period, increasing at an average annual rate of 1.4 per cent to 7 064 PJ in 2035 (Figure 4.4).

Figure 4.4 - Industrial Energy Demand, Reference Case

- The Canadian industrial demand projection is closely related to the economic growth projections discussed in Chapter 3, as well as the projections of oil and gas production. Key trends that impact the Reference Case demand projection include: a gradual recovery in energy-intensive manufacturing industries following the recent economic downturn; strong growth in the oil sands;[14] growth in other natural resource industries such as mining; and, beginning later in the decade, gas production rebounding from recent declines.

- There are various utility demand-side management programs that focus on the industrial sector, as well as federal and provincial programs that aim for energy savings in this sector. These have been maintained or expanded in recent years. These programs can involve improvements in the energy efficiency of devices and equipment, such as more efficient boilers or motors. They may also involve process improvements, equipment maintenance and employee training to enhance energy efficiency and conservation.

- Quebec’s GHG cap-and-trade system is set to begin in 2013, covering large industrial emitters as well as the power sector. It will be broadened in 2015 to include fuel distributors.[15] In 2012 and 2013, the province worked with California in finalizing the link between their carbon markets as part of the Western Climate Initiative. Given these developments, this initiative is included in the Reference Case projections for Quebec.[16] This represents a key change from previous Energy Futures projections.

Transportation Sector

- The transportation sector includes passenger and freight on-road transportation, as well as air, rail, marine, and non-industrial off-road travel.

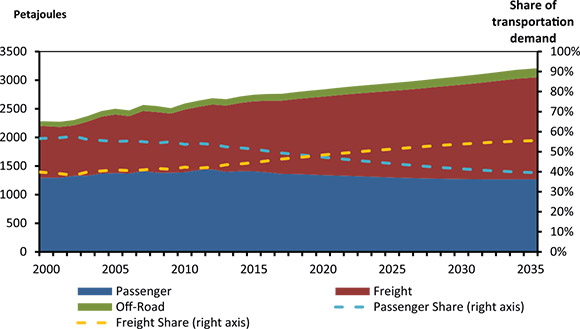

- The transportation sector accounted for 25 per cent of total end-use demand in 2011, or 2 642 PJ. It grows at an average annual rate of 0.8 per cent over the Reference Case projection to 3 210 PJ in 2035 (Figure 4.5).

Figure 4.5 - Transportation Energy Demand by Travel Type, Reference Case

- Growth varies widely between the passenger and freight sectors. With the inclusion of longer-term passenger vehicle emission regulations (covering model years 2017 to 2025), energy demands related to passenger travel declines by an annual average of 0.6 per cent over the projection period.

- Energy demand for freight transportation is driven by growth in the goods-producing industries, and grows at an annual average rate of 2.0 per cent over the projection period. This trend is slower than the 1990 to 2008 historical average of 2.9 per cent per year. This shift is due to somewhat slower economic growth compared to the historical growth rate, as well as federal emission regulations coming into effect for freight trucks (model years 2014-2018). Although these regulations are specified in terms of vehicle emissions, they are expected to reduce future energy consumption by improving vehicle fuel efficiency.

- The 2011 Energy Futures Report included the near-term (2012-2016) passenger vehicle standards, but not the longer-term passenger or freight standards. The inclusion of these regulations in EF 2013 has a significant impact and represents a key change away from the historical trend, as well as from previous Energy Futures projections.

- In 2011, passenger travel accounted for 54 per cent of transportation demand, freight for 42 per cent, and the remainder in non-industrial off-road. In 2020 these shares reverse, with freight accounting for 56 per cent, and passenger for 40 per cent by 2035 (Figure 4.5). As gasoline is used primarily on the passenger side, and diesel in freight, this shift has implications for the use of these fuels. Over the projection period, motor gasoline consumption in transportation declines by 0.2 per cent per year, while diesel consumption increases by 1.6 per cent per year (Figure 4.6).

Figure 4.6 - Transportation Energy Demand by Fuel, Reference Case[a]

[a] Heavy fuel oil is used in marine and rail transportation. Biofuels include ethanol and biodiesel blended with petroleum products. Other includes natural gas, electricity, lubricants and propane.

- Canada’s Renewable Fuels Regulations set a minimum requirement of five per cent renewable fuel content in gasoline starting in December 2010. The regulations were amended to include two per cent renewable content in diesel starting mid-2011.

- Quebec, Ontario, Manitoba, and B.C. have programs and policies to support growth in EV and plug-in hybrid electric vehicles (PHEV), including rebates and pilot projects. In 2035, EVs and PHEVs use four PJ of electricity, or just over one TW.h. This is approximately equivalent to 500 000 EVs and PHEVs on the road.[17]

- There is also interest in natural gas (often LNG) for medium and heavy-duty trucks, particularly in operations where the vehicles return to central locations often and use key regional transport corridors. Several fueling stations are currently being constructed in key strategic highway locations, and several trucking companies have placed orders for natural gas fueled trucks. In the Reference Case, freight NGVs use 100 PJ or 7.4 106m³/d (260 MMcf/d) of natural gas in 2035, representing six per cent of total freight demand. This is approximately equivalent to 60 000 medium- and heavy-duty freight NGVs.[18]

Primary Demand

- Primary demand is calculated by adding the energy used to generate electricity (including hydro, nuclear, and renewable) to total end-use (or secondary) demand, and then subtracting the end-use demand for electricity. Removing end-use electricity demand from the total is necessary to avoid double counting.

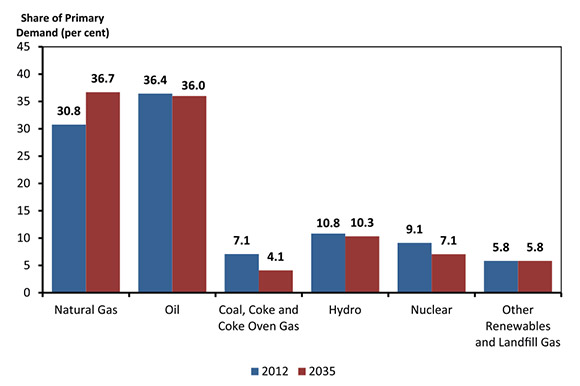

- Primary demand increases at an average annual rate of 1.0 per cent over the projection period. As shown in Figure 4.7, the fastest growing fuel is natural gas, which increases its share of overall primary demand from 31 per cent in 2012 to nearly 37 per cent in 2035. The share of coal and nuclear declines over the projection period, stemming from the electricity projections discussed in Chapter 8. The share of other renewable fuels remains constant, as growth in wind and other non-hydro renewable electric generation is offset by limited growth in end-use biomass consumption.

Figure 4.7 - Share of Fuel in Primary Energy Demand, Reference Case

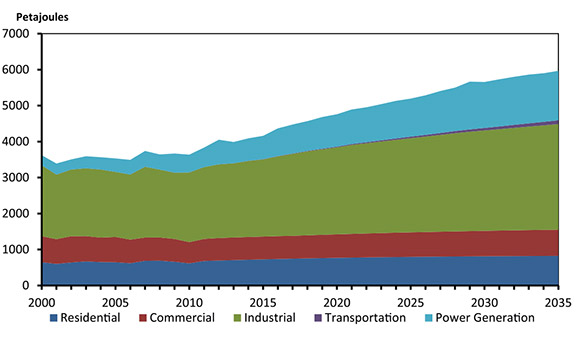

- Natural gas is used heavily in the residential, commercial, and industrial sectors as well as for electricity generation. Figure 4.8 shows primary demand for natural gas, which grows at an annual average rate of 1.7 per cent over the projection period. This is an increase of over 1 900 PJ, or 148 106m³/d (5.20 Bcf/d) over the projection period, with the largest increases in the industrial and power generation sectors.[19]

Figure 4.8 - Primary Natural Gas Demand, Reference Case

Key Uncertainties to the Outlook

- Policies, programs, and regulations are continually under development at federal, provincial, territorial, and municipal levels to meet various government commitments, objectives, and targets. These may have significant implications for energy demand growth. A notable example is the continued implementation of the federal government’s sector-by-sector regulatory approach to reduce emissions. Recent transportation regulations are part of this initiative, and impact the transportation demand projections as described earlier in this chapter. Forthcoming regulated GHG performance standards for other sectors, such as the oil and gas sector, have the potential to affect energy use projections as well.[20]

- In recent years, the oil and gas industry has undergone rapid transformations in both the types of resources extracted, and the technologies used to extract them. Depending on the future development of these resources and technologies, the energy used in this sector may be higher or lower than these projections suggest. As the oil and gas sector is an important energy demand growth area, key uncertainties for the oil and gas production outlooks, described in Chapters 5 and 6, may impact the energy demand projections as well.

- In addition to oil and gas development, the mining sector is a significant natural resource industry for future energy demand projections. A variety of projects are in various stages of development across the country, such as the Ring of Fire developments[21] in Ontario, northern mining developments in Quebec, potash mining in Saskatchewan, and iron ore mining in Newfoundland and Labrador. Energy requirements often vary on a project-by-project basis and are key uncertainties going forward for regional energy demand, particularly electric load growth.

- The Reference Case includes modest penetration of several emerging technologies, such as EV and NGV in transportation, geothermal space heating, and solar hot water heating. Adoption of such technologies beyond the levels included in the Reference Case may change Canada’s future energy use mix and growth.

Chapter 5: Crude Oil Outlook

Crude Oil and Bitumen Resources

- Canada has abundant resources of crude oil, with an estimated remaining ultimate potential of 53.9 109m³ (339 billion barrels) as of December 2012. Of this, oil sands bitumen accounts for 90 per cent and conventional crude oil makes up 10 per cent. Alberta currently accounts for all of Canada’s bitumen resources. Efforts are ongoing to assess bitumen deposits in Saskatchewan, but an official estimate of resource size is not yet available. For conventional crude oil, 72 per cent of the estimated remaining resources are found in the frontier regions that include East Coast offshore, northern Canada and other frontier basins that are still relatively unexplored.[22] The more developed conventional light and conventional heavy oil deposits in the WCSB account for the remaining 28 per cent.

- Resources become reserves only after it is proven that economic recovery can be achieved. Canada has remaining oil reserves of 27.2 109m³ (171 billion bbls) as of December 2012, with 98 per cent of this attributed to oil sands bitumen, and the remaining to conventional oil sources. According to the Oil & Gas Journal,[23] Canada ranks third globally in terms of proven oil reserves, behind Saudi Arabia and Venezuela.

- There is considerable potential to add to Canada’s crude bitumen reserves. The Grosmont Carbonate formation accounts for 21 per cent of the oil sands resources in Alberta. Official recognition of reserves generally awaits proof of economic viability. This recognition may be closer with the approval of the first commercial project in the Grosmont by the Alberta government in July 2013.

- The application of horizontal drilling and multi-stage hydraulic fracturing has provided an opportunity to increase production from previously low-producing or unproductive oil reservoirs in the WCSB. This technology can also potentially be applied to other regions of Canada. While the U.S. EIA recently released a report indicating Canada ranked 10th in the world with 1.4 109m³ (9.0 billion barrels) of technically recoverable shale oil resources[24], these kinds of estimates are highly uncertain at this point in time because this extraction technology as applied to oil reservoirs is still in its early stages in Canada.