Market Snapshot: Fewer natural gas companies operating in western Canada due to technological changes

Release date: 2017-04-26

New technology has reshaped the upstream oil and gas sector. In 2009, over 600 companies operatedFootnote 1 natural gas production wells in western Canada. In 2016, that number had fallen to less than 500 operators despite total natural gas production remaining the same over this period.Footnote 2

Prior to 2009, the majority of companies in western Canada drilled relatively inexpensive vertical gas wells. Modern gas wells are more expensive, since they are deeper, have long horizontal legs, and are stimulated with large applications of hydraulic fracturing. Because these new wells are more costly, smaller operators generally cannot afford to drill new wells. As a result, there are fewer smaller operators in western Canada in 2016 than there were in 2009. Meanwhile, large-size companies can still afford to drill, but often have competing investments, including oil sands projects.

Source and Description

Source: NEB analysis of Divestco well data

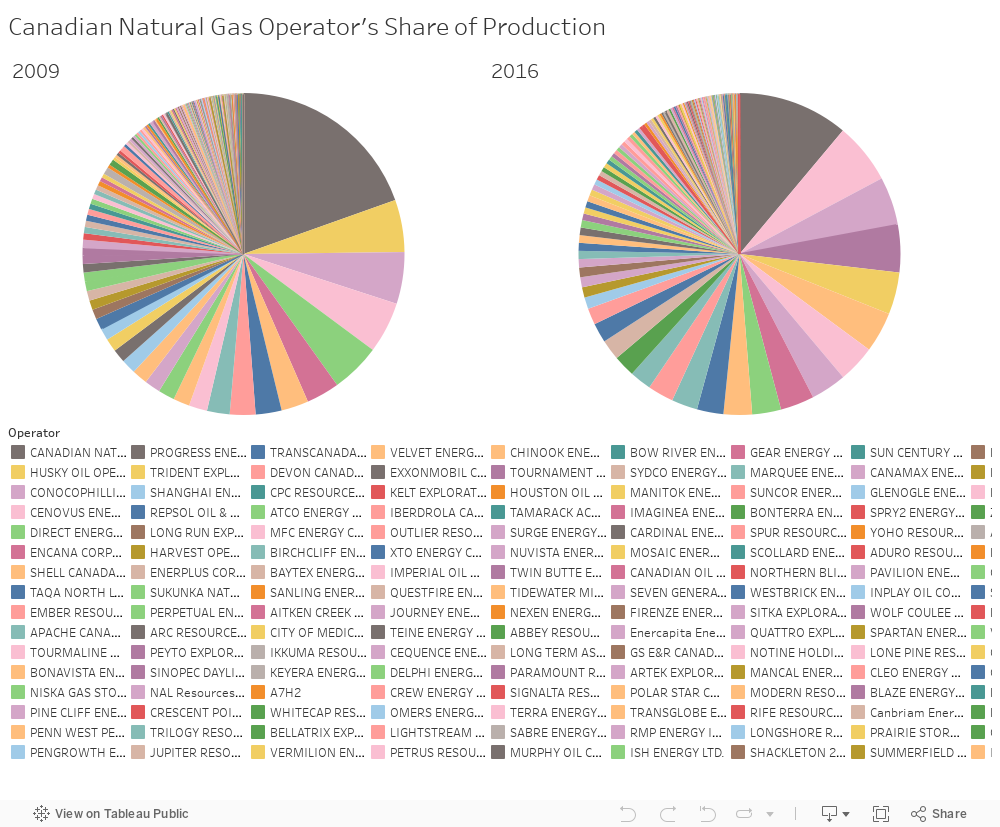

Description: The two stacked charts show each operator’s share of total natural gas production in the years 2009 (left) and 2016 (right), with the size of each bar reflecting their proportionate share of production. The largest operator in 2009 was CNRL at 20% followed by Husky Oil (5%), ConocoPhillips (5%), Cenovus (5%) and Direct Energy Marketing (5%) In 2016 the largest operator was still CNRL, now at 11%, followed by Tourmaline (6%), ConocoPhillips (5%), Peyto Exploration (5%) and Husky Oil (4%).

Even though total production in 2009 and 2016 was almost the same, nine operators accounted for half of total western Canadian operated production in 2009, whereas eleven operators accounted for half in 2016. Meanwhile, 103 operators accounted for 95% of production in 2009, while 81 operators accounted for 95% of production in 2016. This suggests that shrinking production from both the largest and smallest operators has been offset by growing production from medium-sized operators.

The top operators accounting for 50% of production have also changed over the last eight years. Canadian Natural Resources Limited has remained the largest operator, but its share decreased from 20% of total production in 2009 to 11% in 2016. The second largest operator was Husky in 2009, but changed to Tourmaline in 2016, a relatively new operator that started operations in 2008. ConocoPhillips was the third largest operator in both years.

- Date modified: